Japanese beauty house Pola Orbis Holdings Group celebrates its 90th anniversary this year, a landmark that coincides with a newly outward-looking perspective as the company seeks to extend its international horizons.

The reasons for such expansion are clear. Business at home is tough. The beauty category within Japan has become intensely competitive with new brands constantly entering the country’s once insulated cosmetics market. All those brands are communicating louder than ever before at both retailer and direct-to-consumer level.

Excluding strong consumption by inbound tourists, Japan’s cosmetics market shrunk in 2018. In contrast, Pola Orbis Holdings Group’s overseas markets continued a modest expansionary trend, buoyed by firm growth in Asia, especially China.

In a message to shareholders this March, President Satoshi Suzuki signalled his intentions, commenting: “Under these market conditions, the Pola Orbis Group took steps to improve the profitability of its operations in Japan, move its overseas operations into the black and develop next-generation growth brands in accordance with its medium-term management plan for the four-year period from 2017 to 2020, which was launched in 2017.

“In the global market, we intend to accelerate shop openings, especially in China, and increase our brand presence,” said Suzuki. “We are united in our determination to realise our 2020 long-term vision of becoming a highly profitable global enterprise and achieve further rapid growth.”

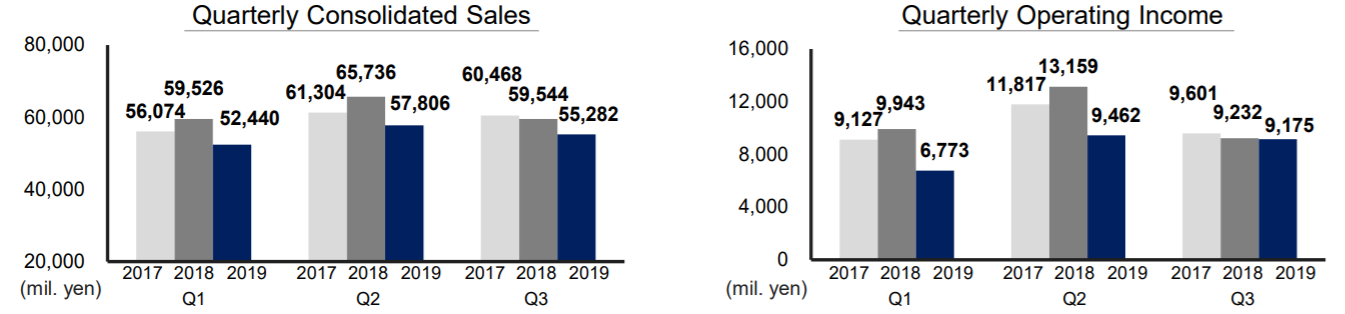

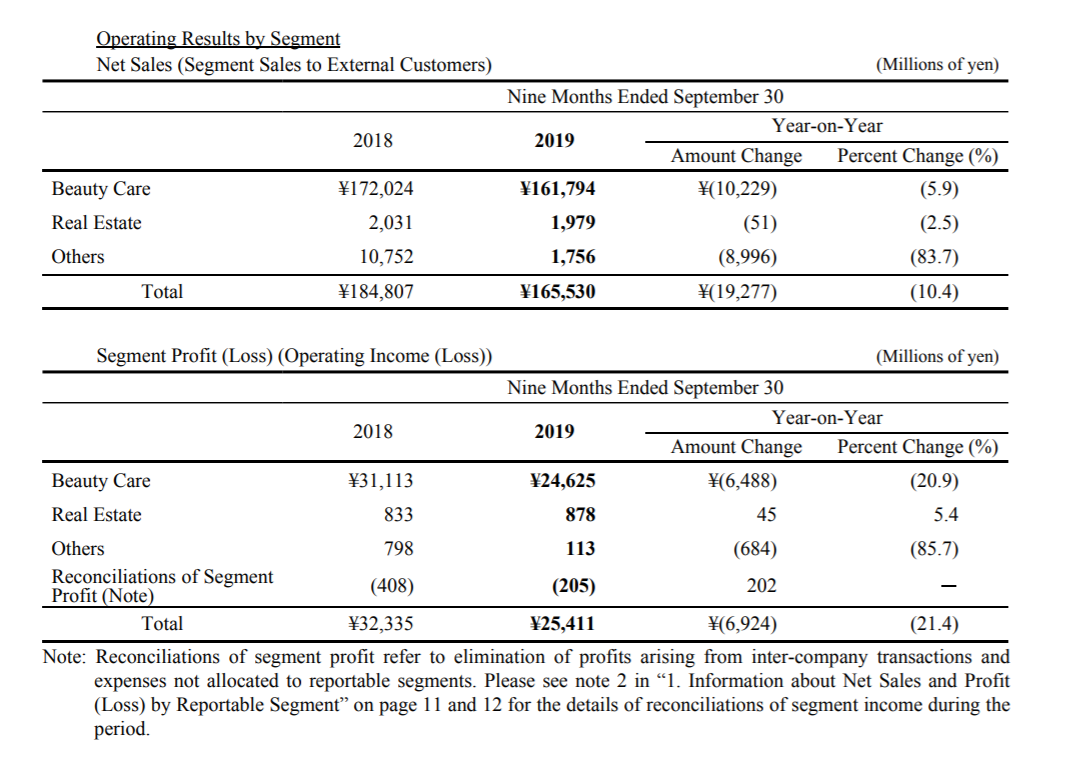

But as the group’s nine-month results (see chart below) show, business at home has continued to struggle. And for a company that generates 90% of its revenue from its domestic market, that makes the need to internationalise even more urgent.

Travel retail, that inherently international channel, has been identified as a particularly strong opportunity to build the group’s global presence. To discuss that opportunity and wider market prospects, The Moodie Davitt Report Founder & Chairman Martin Moodie and Fashion, Beauty & Social Media Editor Hannah Tan-Gillies sat down with Pola Orbis Holdings Group Director and Vice President Naoki Kume at the recent TFWA World Exhibition in Cannes. Kume-san was joined by Jurlique International Markets Managing Director Benoît Wagner. It was the group’s first visit to the Cannes show, testament to a renewed commitment to the channel.

Reflecting that focus, the group has just opened new Jurlique and Three counters at Beijing Daxing International Airport in partnership with China Duty Free Group– with more Chinese counters planned in the near future. In this compelling interview, Kume-san discusses the group’s multi-brand strategy, the role of the Chinese market, the rise of clean beauty, and the need for both incubation and innovation. He also stresses the importance of group synergy, amid moves to develop Jurlique Pola, Orbis and Three in travel retail.

You are here in Cannes for the first time. What role does travel retail play for the company and how do you see this evolving?

We recognise that the travel retail market is growing globally, particularly in Asia Pacific. We also know that the channel’s growth is linked to the growth of domestic markets in Asia, and so we plan to grow both channels in tandem.

Both domestic and travel retail markets in Asia are focusing heavily on skincare; and so, we are looking to match our strengths as a group with Asia’s growing skincare trend. This is why we’ve made the decision to push our four strongest skincare brands into travel retail: Jurlique, Pola, Orbis and Three.

Pola Orbis Holdings has a very distinctive multi-brand strategy, especially with those four brands you mentioned. How does that philosophy play out in travel retail?

Each brand is quite independent from each other; and the target consumers are different too. However, it’s much better for us to utilise group synergy for our travel retail strategy, especially when negotiating with operators and distributors. This is why we’ve brought the top two people from each brand to Cannes. We wanted them to learn and understand how to approach the channel moving forward.

As you said, Jurlique, Pola, Orbis, and Three have different positionings. How would you position Jurlique today – and how do you see the brand developing?

When we acquired Jurlique in 2012, there were many natural brands that were available for M&A. However, we weren’t just looking for any natural brand, but one that was thoroughly natural and also had a very clear character. Jurlique stood out because it had its own farm, and because the brand’s ‘seed-to-skin’ concept really resonated with us.

Another reason for acquiring Jurlique was that it already had a strong presence in China and in travel retail. At the time, we didn’t have anything like that within our own portfolio, so we thought this would be a great complement to our group. We also thought the acquisition would help us gain some insight into the Chinese market, particularly through the brand’s existing networks in China and Beijing. At the time, Jurlique already had a relationship with China Duty Free Group, which is one of the reasons we were able to recently open both Jurlique and Three in Beijing Daxing Airport.

Getting Three into Beijing Daxing was a success story of our synergy with Jurlique. Now we want to launch Pola and our other brands into China and expand into other key Chinese airports too.

Is M&A still a priority for the group?

M&A is still high on our list of priorities, because as you mentioned earlier, we have a very distinctive multi-brand strategy. We see two ways of developing that strategy, the first is M&A, and the other one is to incubate our own brands. Three is the best example of the latter.

Can you leverage Jurlique’s seed-to-skin clean beauty concept across different regions – especially with the global rise of the clean beauty trend?

In Europe there is a lot of demand for biodynamic beauty, and North America is even more extreme with the clean beauty trend. We currently have a subsidiary in the US, and we’re growing more than +50% in the region.

I think Jurlique has huge potential in Europe. We’re working on expanding there, even if the centre of gravity of the beauty industry is currently in Asia. There are plenty of consumers looking for exactly this kind of product; natural, Australian, and with the seed-to-skin concept. We are currently in discussions to expand into Greece, Denmark and the United Kingdom.

What has been the biggest for Jurlique since being acquired by POAG? What are the key areas of focus for the brand?

Benoît Wagner: We have been very focused on maintaining Jurlique’s origins, values, and naturality. Since joining the group, we have shifted our focus towards creating more hero products in skincare. We are currently highlighting the Activating Water Essence and the Nutri-Define anti-aging line, which will be re-launched in January 2020.

Amongst all of our brands, Jurlique has the most experience and exposure in travel retail, that’s why we’re very happy to share our experience and knowledge with the group. In recent years, we’ve worked towards further communicating the naturalness of Jurlique and leveraging its popularity in the channel. We’ve reworked our packaging and also launched a new retail design in Beijing Daxing Airport, Hong Kong International Airport, and in domestic markets as well.

Our main areas of focus are China, Australia, Hong Kong and Japan. Travel retail has a big share in the market, as it’s in the top four or five markets for us. However, China represents more than 50% of our market, as the core consumer of Asian travel retail is Chinese. We currently have a mixed distribution subsidiary in China but are aiming to have 100% control of our Chinese distribution by the end of the year.

Is Pola a priority brand in your travel retail expansion? How do you see it evolving in the channel?

Pola is our flagship brand. We’re making big investments to increase our doors in China and open more counters in both downtown duty free and airport stores in travel retail.

We already have a pretty successful travel retail business in South Korea. It’s grown tremendously in recent years because that’s where Chinese tourists go to buy duty free products. Looking at the Daigou phenomenon, we can assume that the Chinese government may try and prioritise domestic consumption. Because of this, we see expanding into more Chinese airports as a tremendous opportunity for Pola.

Chinese CFDA regulations are quite unique, so as far as our offshore development is concerned, there is still plenty of room to grow. With airports however, there are more immediate features such as cross border e-commerce, where those CFDA regulations may not apply – which is another opportunity for growth.

How do you see the daigou phenomenon evolving? Is it a business that will continue to grow? Or do you see it as a business that the Chinese government will try to regulate even more?

The new e-commerce regulations say that as long as the Daigou pay tax, the business will continue to grow. Therefore, unless something really destructive happens in the near future – we see the Daigou’s future as quite good.

The strength of the Daigou is that their knowledge of the market is formidable. So, as long as they don’t do any damage to the brands, we are happy to benefit from this phenomenon.

Alibaba Group and Tmall’s new ‘Fliggy Buy’ concept is a very interesting example of how the direct-to-consumer business in China is changing. Could you tell us more about your direct-to-consumer business in China?

The good thing about our direct-to-consumer business in China is that our customers are able to try our products for themselves. Through some personalised skin consultations, our clients can really see what’s best for their skin. At the moment, we are exploring how we can create a high-quality advisory function like this for online, but that’s yet to come.

What about Orbis? Where does the brand stand today and how will it grow in the future?

Orbis has a very mature market in Japan. It has grown into a ¥50 billion (US$4,608 million) brand in the domestic market. It was a pioneer in the online and direct market model, but has plateaued in recent years.

Japanese consumers are very demanding. If a brand is successful in Japan, that becomes a precursor for success in other markets too – especially in China. The reason Japanese brands are so popular in China is because they are synonymous with high-quality and effective products – both qualities are present in Orbis too.

Orbis is a tried and tested Japan-grown brand. Japanese online sales currently hold the biggest weight for Orbis, but I can see plenty of opportunity for it to grow in China too. At the moment we are looking to expand Orbis into Chinese domestic markets only through online sales.

90% of Pola Orbis Holding’s revenues come from the Japanese domestic market. Now that you are expanding into travel retail – how do you see your local v international mix evolving?

Yes, 90% of our revenue currently comes from the domestic market. However, our international sales ratio outside of Japan is also growing; and we believe that travel retail is the driver.

Because where else in the world can you find a market that grows 30% a year? With that in mind, we’re definitely focusing on travel retail, and more specifically Asia Pacific travel retail in the years to come.

You mentioned that you were incubating Three. Could you elaborate?

The first part is internal incubation. We have a system in place wherein employees are encouraged to propose new business ideas. As long as the board approves these ideas, we really try to implement them.

Our secondary incubation strategy is putting minority investments into early stage ventures. If it is a really good concept, then we will aim to acquire either 100% of the company or become a subsidiary. We have already invested into a variety of early stage companies outside of cosmetics. We’ve also made investments into beauty technology and retail technology companies that will hopefully strengthen our foothold in other business areas.

If you had one message to present to the travel retail world about the group – what would it be?

Our message would be that we do realise we are entering the market quite late but appreciate its importance. We are ready and determined to invest our resources in the channel and are looking forward to creating great partnerships within the travel retail industry.