INTERNATIONAL. Welcome to the sixth edition of the Moodie Davitt SPEND Index, a platform that tracks the effects of currency fluctuations across leading travelling nationalities and destinations – a key driver of travel retail spending.

Among all the factors affecting travel between nations, exchange rates are one of the most important, as they are central to determining relative spending power.

Our Moodie Davitt SPEND Index continues to track the effects of currency fluctuations across selected travelling nationalities and destination countries – a key driver of spending in travel retail.

The SPEND Index examines the changing value of selected home currencies against other currencies abroad. That carries significant weight when it comes to decisions about whether or where to travel, and travellers’ propensity to shop while overseas.

By the latest count, there are 162 world currencies that are traded on a daily basis. The number of combinations of currency pairs comes to 26,082, a number big enough to keep every forex trader busy 24/7.

Some currencies and currency pairs are, of course, more important than others. Assuming that the sales transaction is made in the currency of the country where the shopping takes place, the US Dollar (including currencies pegged to the greenback) is used in approximately 40% of global duty free and travel retail sales transactions, followed by the Euro with a 25% share. The Korean Won comes third at 10% followed by the British Pound at 7% and the Chinese Yuan with a 6% share. Thus the 157 remaining currencies – including most notably the Brazilian Real, the Russian Ruble, the Japanese Yen, the Australian dollar and the Swiss Franc – together have a 12% share.

The SPEND Index naturally includes the top five currencies, representing approximately 88% of global duty free and travel retail sales. In addition, it features ten other currencies, together embracing 15 of the most common currencies in global travel retail.

In previous editions of the SPEND Index we have focused on nationalities. This time we focus instead on the destination countries that have become more attractive and more favourable in terms of visiting and as a shopping destination. We also give attention to the countries that have become less attractive and less favourable to visit due to changes in the rates of exchange in the past 12 months. Exchange rates on 30 September 2019 have been compared to those of 30 September 2018.

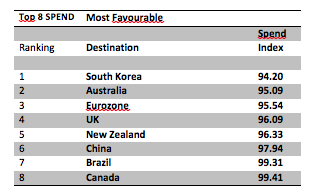

The destinations that enjoy an increased spending power (“Most Favourable”), based on the evolution (i.e. weakening) of their domestic currency over the past 12 months (up to 30 September 2019) versus a basket of other currencies, are listed below.

A SPEND Index of less than 100 (“Most Favourable”) indicates that the spending power of visitors to this country has improved over the past year due to a weakened currency in the country of destination. Likewise, a SPEND Index greater than 100 (“Least Favourable”) indicates that shoppers’ spending power in this country has weakened due to a strengthened currency in the country of destination.

Given exchange rate fluctuations, the country that has benefited the most over the past 12 months (see the table above) is South Korea (rank 1, SPEND Index 94.20). Visitors and duty free shoppers in South Korea are making a saving of 5.8% on average (all visiting nationalities) compared to one year ago.

South Korea is the world’s most important duty free and travel retail market with a share of about 10% of the global market. As reported, in the month of July South Korean duty free sales climbed by +27.7% year-on-year maintaining its strong 2019 growth trajectory. The depreciation of the South Korean Won has certainly contributed to this impressive growth so far in 2019.

The South Korean duty free market is heavily dependent on international customers (mainly Chinese, representing slightly more than one third of all visitors); international customers outnumber South Korean customers at a ratio of about 5 to 1. In the period January to July 2019, the number of visitor arrivals to South Korea grew by +16.7% on average. Visitor arrivals from China soared at a growth rate of +27.5% during the same period.

Whilst South Korea is currently ranked as the most favourable country to visit, and to shop, the negative aspect to this is of course that South Korean’s spending overseas has suffered. According to UNWTO, in the first half of 2019 South Koreans globally spent -8.0% less than during the same period one year ago, partly due to the depreciation of the South Korean Won.

Weakened currencies in Australia (rank 2, SPEND Index 95.09, saving 4.9% on average, all nationalities of visitors), Eurozone (rank 3, SPEND Index 95.54, saving 4.5%) and the UK (rank 4, SPEND Index 96.09, saving 3.9%) today welcome visitors and shoppers that all enjoy an enhanced spending power compared to one year ago.

With a SPEND Index at 96.33 as for New Zealand (rank 5, SPEND Index 96.33), a basket of products that cost NZD (New Zealand dollars) 100.00 on 30 September 2018 now only costs NZD 96.33 on average (all visitor nationalities), a saving of 3.7%.

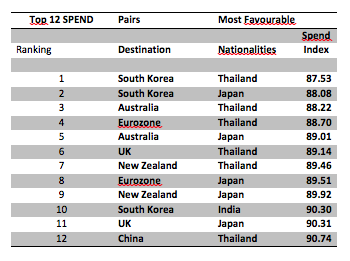

The SPEND Index also offers the possibility to study details and numbers between pairs of destination countries and nationalities. Destinations are given as countries rather than cities (see table below).

Evidently, the nationalities that have benefited the most from their strengthened currency are those from Thailand and Japan in particular.

Over the past year, given the exchange rate movements between the South Korean Won and the Thai Baht, the table above shows that South Korea has become the most favourable destination for duty free shopping for Thai travellers. With a SPEND Index at 87.53, Thai travellers now make a significant saving of 12.5% when visiting and shopping in South Korea.

Thai travellers also make significant savings in five additional countries (see table above), including the UK (rank 6, SPEND Index 89.14, saving 10.9%). In the month of August, Thai shoppers visiting the UK spent +43.0% more on average per transaction year on year, according to Global Blue.

Japan is an important source country of visitors to South Korea representing 19.7% of all visitors during the period January to August 2019, up +22.0% year-on-year [Source: KTO]. Today Japanese visitors (rank 2, SPEND Index 88.08) make a saving of 11.9% on their duty free purchases in South Korea compared to one year ago.

Favourable destinations to the Japanese are also Australia (rank 5, SPEND Index 89.01, saving 11.0%), the Eurozone (rank 8, SPEND Index 89.51, saving 10.5%), as well as New Zealand and the UK. According to UNWTO, in the first half of 2019 Japanese spending overseas increased by +11.0%.

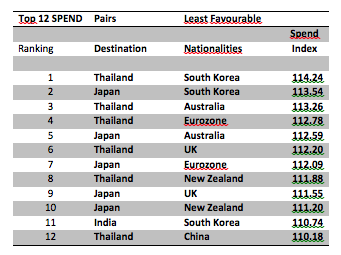

The destination countries that have lost and suffered in terms of visitors’ declining spending power appear in the table below.

The above seven countries have all seen their currencies strengthen over the past year making them – from a rate of exchange point of view – less attractive as destination points as visitors’ spending power has decreased.

Duty free shopping in Thailand (rank 1, SPEND Index 108.63) has become 8.6% more expensive on average (all visiting nationalities) over the past 12 months. The Association of Thai Travel Agents (ATTA) says the number of visitors to Thailand is down -6.6% in the year to date (up to 30 September 2019).

It is yet unclear to what extent the ongoing Rugby World Cup has boosted the number of visitor arrivals in Japan, despite the “more expensive” Japanese Yen which over the past year has gained +7.9% on average (rank 2, SPEND Index 107.92) against the 14 other currencies in the SPEND Index basket.

The 48 matches in the Rugby World Cup, ending with the final on 2 November, are expected to attract some three million attendees to the arenas where the games are played, many arriving from overseas.

The list below shows some of the countries involved in the Rugby World Cup 2019 and how much their currencies have lost in value to the Japanese Yen in the past 12 months:

- AUD / Australian dollar -11.2%

- CAD / Canadian dollar -7.4%

- EUR / The Euro -10.8%

- GBP / British pound -10.4%

- NZD / New Zealand dollar -10.1%

- RUB / Russian rouble -3.8%

- USD / US dollar -5.0%

If the Japanese Yen continues to strengthen, this may be to the detriment of the number of visitors expected for the Olympic Games scheduled to be held in Japan between 24 July and 9 August next year. Overseas visitors to the Olympic Games might not have the same cost tolerance and acceptance as the passionate and hardened aficionados attending the Rugby World Cup this year.

Thailand and Japan dominate the “Least Favourable” destination list entirely due to the strengthening of the two countries’ currencies. As the table above shows, several nationalities now find it more expensive to visit and shop in Thailand.

The fact that Thailand so far in 2019 has become a less popular destination is supported by the latest data (1 January 2019 to 30 September 2019) from ATTA. Their data corresponds very well with the SPEND Index.

Extracting the six nationalities in the table above listed alongside Thailand as a destination unveils:

- South Korean (rank 1, SPEND Index 114.2) visitors to Thailand now pay 14.2% more when shopping in Thailand. According to ATTA, during the first three quarters of 2019, the number of South Korean tourist arrivals has dropped by -12.2%.

- Australian and New Zealand visitor arrivals (rank 3 and 8), with SPEND Index 113.26 and 111.88 respectively, have seen a decrease (both countries combined) in arrivals in Thailand of -16.6%.

- Eurozone (rank 4), the SPEND Index equals 112.78; tourist arrivals are down -15.5%.

- The UK (rank 6), the SPEND Index equals 112.20; tourist arrivals in Thailand have dropped a very significant -30.6%.

- China (rank 12), with a SPEND Index equalling 110.18, tourist arrivals have declined by -6.8%.

According to the ATTA statistics, the total number of tourist arrivals in Thailand in the first three quarters of 2019 is down -6.6% against the same period in 2018. This can be compared to the SPEND Index for Thailand, as a destination country, which stands at 108.63 on average (all nationalities of visitors).

This effectively means that Thailand has become +8.6% more costly to visit (including shopping) on average, resulting in a -6.6% decrease in tourist arrivals. This confirms the long-established theory that a ‘strengthened’, ‘strong’ or ‘overvalued’ – whichever term one wishes to use – currency has an adverse effect on a country’s duty free and travel retail business; that it has a negative impact on the tourism and travel sectors overall as well as that it represents major challenges to a country’s export industry on the whole.

The Moodie Davitt SPEND Index analysis embraces 210 nationality and country of destination pairs, as well as 15 averages each for nationalities and destinations (= 240 x value indicators). It will continue to monitor the consequences and possible impacts of currency fluctuations on duty free and travel retail trade in the months ahead.

PREVIOUS EDITIONS OF THE SPEND INDEX