INTERNATIONAL. Welcome to the third edition of The Moodie Davitt SPEND Index, a platform that tracks the effects of currency fluctuations across leading travelling nationalities and destinations – a key driver of travel retail spending.

The value of the domestic home currency against other denominations abroad carries serious weight when it comes to consumers decisions whether to travel, where to travel and, of course, if, how, and where they shop.

The SPEND Index embraces 15 of the most common currencies used in global duty free and travel retail.

The nationalities that enjoy an increased spending power (‘Winners’), based on the evolution of their domestic currency over the past 12 months (up to 30 September 2018) versus a basket of 14 other currencies, are listed below.

A SPEND Index <100 indicates that the spending power of this nationality has improved over the past year due to a stronger currency. Likewise, a Spend Index >100 indicates that the spending power of this nationality has weakened due to a weaker home currency.

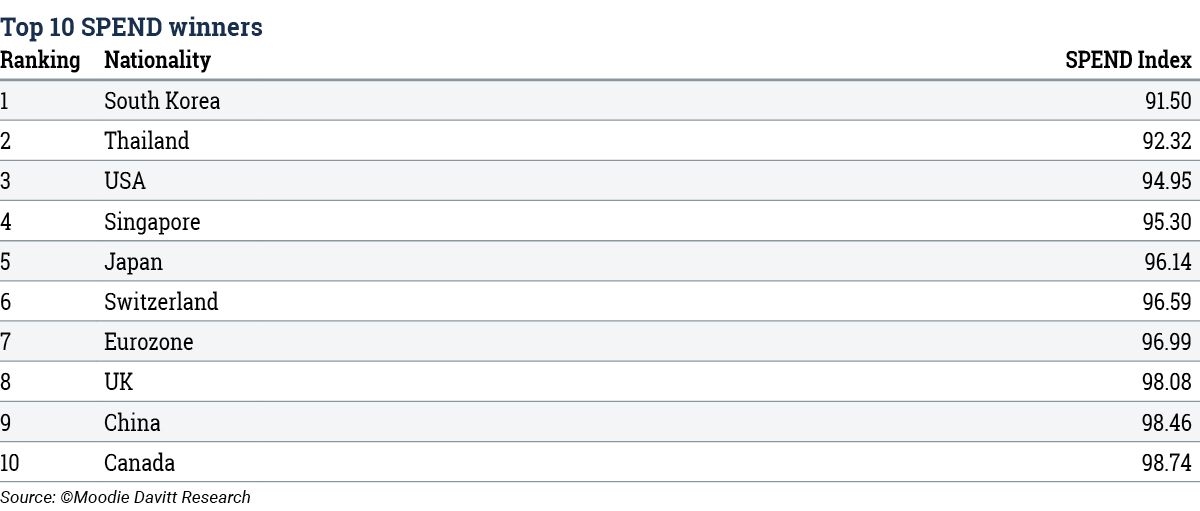

The nationalities that have benefited the most over the past year from a strengthened currency are those from South Korea, Thailand, the USA, Singapore, Japan, Switzerland, the Eurozone, the UK, China and Canada. Currency values and rates of exchange on 30 September 2018 have been compared to those valid on the same date in 2017.

With a SPEND Index of 91.50, as for South Korea, a basket of products that cost KRW100.00 on 30 September 2017 now only costs KRW91.50 on average (all countries and destinations), a saving of 8.5%.

The strengthening of the Korean Won (KRW) over the past year can largely be attributed to expectations of forthcoming economic reforms led by President Moon Jae-in and the fact that recent economic data has turned out much better than forecast. To this can be added the widely accepted view that the Won over the past nine years has been kept artificially undervalued by government interventions in order to promote exports and support local companies.

The recent weakening of the Chinese Renminbi against the greenback (from early April to 20 November, the Chinese currency has fallen -10% against its US counterpart) has profound implications for Chinese spending power in any Dollar-based, Dollar-linked or Dollar-influenced travel retail location.

The Thai Baht has increased in value over the past year. Overseas Thai travellers now spend on average -7.7% (SPEND Index = 92.32) less on their duty free and travel retail purchases compared to one year ago.

US travellers have benefited from a strengthened US Dollar over the past 12 months; it has gained in value against all currencies in the basket except the Korean Won. On average, US travellers now make a saving of -5% (SPEND Index = 94.95) on their duty free and travel retail purchases compared to one year ago. The US Dollar strength can be attributed to a booming domestic industry with significant GDP growth rates, low unemployment figures, as well as other positive economic data.

The US Dollar is the most critical currency in the SPEND Index. The recent weakening of the Chinese Renminbi against the greenback (from early April to 20 November, the Chinese currency has fallen -10% against its US counterpart) has profound implications for Chinese spending power in any Dollar-based, Dollar-linked or Dollar-influenced travel retail location.

The SPEND Index also offers the opportunity to study details and numbers between the pairs of ‘nationality’ and ‘country of destination’.

Plummeting Brazilian Real hurts spending power

Over the past year the Brazilian Real (BRL) has weakened against all other currencies in the basket. Thus, all nationalities visiting Brazil make a saving averaging -18.9% (SPEND Index = 81.06) when shopping in any Brazilian duty free shop. The savings range from -24.2% made by visiting South Koreans to -10.7% for Russians visiting Brazil. Conversely the Brazilian consumer’s spending power when travelling has plummeted.

South Koreans going to Russia (SPEND Index = 84.91) now benefit from a -15.1% price reduction on duty free purchases in any Russian duty free shop compared to one year ago. Russia might also be an attractive shopping destination for Thai travellers (Spend Index = 85.20) as they now shop at -14.8% cheaper duty free prices than at the same time last year.

Below is an analysis of nationalities and currencies that have suffered over the past 12 months.

The nationalities that have lost in terms of their spending power are:

The above five countries, and outbound travellers from these countries, have all seen their currency weaken, effectively meaning that today their currencies have less worth than one year ago. Focusing on Brazilian travellers, with a SPEND Index at 123.62, a basket of products that cost BRL100 on 30 September 2017 now costs BRL123.62 on average (all destinations), a significant increase of +23.6%.

On 30 September 2018, 4.05 Brazilian Reals bought 1.00 US Dollar. This compares with July 2011 when just 1.67 Reals bought the greenback. The strength of the Real was then backed by strong economic growth in Brazil which also fuelled the duty free business there as well as in neighbouring countries at the time. This impact could be seen all the way up to the US east coast, even to Europe, with these locations seeing increasing numbers of high-spending Brazilians travelling.

As Brazil lacks a stable, robust and reliable currency, the volatility and depreciation of the Brazilian Real in recent years has been one of the major worries and concerns of investors as well as duty free retailers in the region. In its first half 2018 report, Dufry – the largest duty free retailer in Brazil (and the world) – noted: “The devaluation of the Brazilian Real and the Argentinean Peso are affecting our sales in US Dollars. Having said this, when measured in local currencies, the performance of the business is stable, which is a sign that the overall consumer sentiment is still positive.”

This comment suggests that Brazilians travelling to destinations abroad are still buying duty free in domestic (rather than overseas) duty free shops upon departure where they can get greater value currently.

Russians travelling abroad have over the past year seen their duty free purchases become +9.7% (SPEND Index = 109.69) more expensive on average calculated in the Russian Ruble.

Indian Rupee weakens

Travellers from India, likewise, are now facing +6.5% (SPEND Index = 106.46) higher duty free prices on average compared to one year ago due to the weakening of the Indian Rupee over this period.

Focusing on ‘nationality’ and ‘country of destination’ pairs, the table below show the combinations and nationalities and destinations that have suffered the most.

Due to the significant weakening of the Brazilian Real over the past 12 months, the 14 country destinations monitored here for Brazilians going abroad have all become more expensive by an average of +23.6% (SPEND Index = 123.62). The list of more expensive duty free shopping destinations for Brazilians range from South Korea, where Brazilians now pay +31.9% more than 12 months ago, to Australia, where prices calculated in the devalued Brazilian Real have become +17.8% more expensive.

Reduced Ruble value undermines Russian spending

Russians travelling to South Korea, Thailand and the USA have seen their spending power reduced as they are now paying substantially more for their duty free purchases (South Korea at +17.8%; Thailand at +17.4%; and the USA at +14.5%).

In recent years Russian travellers have become important spenders in duty free and travel retail shops in Europe and Southeast Asia especially. Their level of travelling and spending in duty free and travel retail shops are and have been predominantly tied to the value of their currency. A weakened Ruble obviously negatively affects Russians’ frequency of travel and choice of destinations as well as their spending in shops.

Over the past year the Russian currency has continued its slide against other major currencies, against a background of European and US sanctions against Russia. There have also been mounting fears that the Russian economy is heading for recession.

The Moodie Davitt SPEND Index analysis embraces in total 210 nationality and country of destination pairs as well as 15 averages for nationalities (= 225 value indicators). It will continue to monitor the consequences and possible impacts of currency fluctuations on duty free and travel retail trade in the months ahead.

PREVIOUS EDITIONS OF THE SPEND INDEX