AUSTRALIA/NEW ZEALAND. Ivo Favotto, a Sydney-based executive and company owner who has worked for all three stakeholders in the Trinity chain, presents the latest figures commentary on the gradual re-emergence of airport commercial activities in Australia and New Zealand. Favotto owns and runs The Mercurius Group, a consultancy focused on industry research, consultancy and benchmarking studies, as well as operating his own destination merchandise supply business.

AUSTRALIA/NEW ZEALAND. Ivo Favotto, a Sydney-based executive and company owner who has worked for all three stakeholders in the Trinity chain, presents the latest figures commentary on the gradual re-emergence of airport commercial activities in Australia and New Zealand. Favotto owns and runs The Mercurius Group, a consultancy focused on industry research, consultancy and benchmarking studies, as well as operating his own destination merchandise supply business.

Here, Favotto considers the manifold challenges faced by foreign exchange providers in Australasian airports, led by the falling number of cash transactions in retail and the rise of electronic payment methods. Their challenges, he notes, are accelerating due to concerns about COVID-19 virus transmission through cash handling.

He warns that airport currency exchange concessions are at risk of being caught in a classic pincer movement – reducing cash reliance on the left flank and price transparency driven by internet-based competition on the right.

Across Australia and New Zealand, currency exchange concessions at airports were already struggling in pre-COVID-19 years with the global shift of consumer payments to credit card and mobile device-enabled payment systems. The health-driven push for contactless payment during the current coronavirus crisis may well prove to be the final nudge that sends these concessions over the edge and into oblivion.

Currency exchange concessions are – or at least were – very good earners for many airports and have been for a long time. For some airports, the per-square-metre returns of high turnover/small footprint currency exchange concessions often rivalled the fabled per-square-metre returns of duty free concessions. And in absolute terms, currency exchange concessions were often the highest individual rent payers of all forms of specialty retailing (excluding duty free of course).

“The days of airport currency concessions churning out rivers of cash for airports are fast disappearing”

This was especially true of airports where the passenger nationality mix generated demand for currency exchange involving higher margin exotic currencies (the thinly traded and more illiquid or volatile currencies).

But the days of airport currency concessions churning out rivers of cash for airports are fast disappearing.

There are two key factors behind this. First is the gradual shift in consumer payment preferences away from cash and towards a growing array of non-cash options including credit/debit cards (increasingly with tap-and-go features) to newer-age mobile-based technologies such as Apple Pay, Paypal, UnionPay, WeChat Pay and AliPay. And second is the evolution of competition in currency exchange markets.

Changing consumer preferences

According to a recent report by Reserve Bank of Australia (the RBA is Australia’s central bank) – Consumer Payment Behaviour in Australia 2019 – only 27% of all consumer transactions in Australia (by volume) were made in cash, down from 69% in 2007. By value, the decline is even more dramatic, with cash use accounting for just 10% of the value of consumer transactions.

The shift is most pronounced in the under-30 age group, where cash accounts for less than 15% of transactions and in higher income households where cash accounts for only around 21% of transactions.

Whereas cash used to have a significantly higher share in small transactions of less than A$10 – more than 90% in 2007 – the majority of even these transactions (55%) have now gone cashless given the widespread uptake of tap-and-go technologies like Visa’s PayWave.

In the RBA 2019 study, a whopping 36% of consumers reported never using cash for point-of-sale payments – up from around 3% in 2007.

The flip-side of the decline of consumer cash usage is the inexorable rise of credit card usage, now accounting for 63% of all transactions by volume and even more by value. Interestingly, debit card usage has surged while credit card usage has ameliorated.

A similar story emerges from New Zealand in a recent study published by Reserve Bank of New Zealand (Cash Use in New Zealand, 2019). In this study, 89% of consumers reported a strong preference to always pay by non-cash methods.

This is supported by additional findings in Cap Gemini’s World Cash Report, 2018 that records New Zealand as having one of the lowest and most rapidly declining ATMs (automatic teller machines) per capita in the world (around 70 per 100,000). New Zealand has one of the fastest falling bank branches per capita in the world.

From a global perspective, the flight from cash is by no means universal. But neither are Australia and New Zealand outliers. Noting that the Cap Gemini report relies on 2018 data (with anecdotal evidence suggesting the pace of switching to non-cash is fast accelerating), other countries that are experiencing cash’s share of consumer transactions falling include:

- South Korea – cash share of transactions, 15%;

- Sweden – cash share of transactions, 20%;

- USA – cash share of transactions, 32%;

- UK – cash share of transactions, 42%.

And all this is before COVID-19. In April 2020, the Bank of International Settlements issued a report highlighting that COVID-19 had raised an unprecedented amount of concern about virus transmission through cash handling. Many retailers across Australia and New Zealand have gone cash free – at least for now.

Whether they go back remains to be seen, as for many retailers, there are material operating cost savings in going cashless, not to mention the risk minimisation benefits (cash has a habit of getting “lost” and/or stolen). COVID-19 may well accelerate the push for early adopter countries like Australia and New Zealand to become totally cashless although much debate ensues about if and when this will happen.

Notwithstanding cash’s decline as a means of transacting, some observers have noted that cash-in-circulation (as a percentage of GDP) is rising. This suggests an increasing use of cash as a store of value in the current low interest rate environment in many countries and given economic uncertainties posed by the COVID-19 outbreak. There may be many a mattress stuffed with cash around the world right now.

Evolving nature of competition in currency exchange

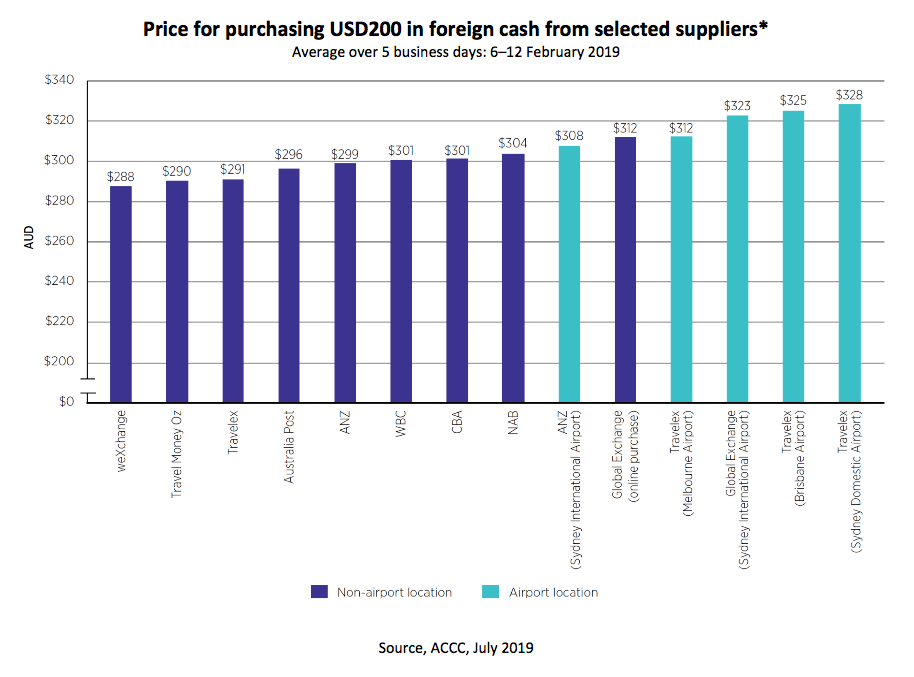

On top of the global move to non-cash transactions, in July 2019 the Australian Competition and Consumer Commission (ACCC) issued the final report of its Foreign Currency Conversion Services Inquiry.

The ACCC inquiry was driven by concerns over the lack of transparency and the complexity of currency exchange services prices. The ACCC found that “payment cards are generally cheaper than foreign cash and travel cards” and “prices for foreign cash were substantially higher at the airport”.

The ACCC Report highlighted that the highest price at Sydney Airport for purchasing US$200 was A$40 higher than the lowest price on the market.

The ACCC noted some submissions to the inquiry argued that the airport price premium was due to the airport being a convenience offer and that airport occupancy costs (i.e. rents, trading hours etc) were typically higher than in other locations.

The ACCC also noted that price premiums were also driven by information asymmetry (i.e. consumer ignorance), consumer apathy and even information opacity for consumers (i.e. making it hard to figure out prices and differences in prices). All of which is nothing new and not necessarily limited to currency exchange services.

Moreover, the ACCC noted that growing competition, in particular from non-bank and online foreign currency services was improving transparency and was driving down retail margins charged by operators at airports. At the same time, the ACCC reported that while reducing retail margins did elicit a demand response from consumers (i.e. consumers bought more as prices came down), the demand response was not enough to make the move margin-neutral.

Implications for airport currency exchange concessions

Airport currency exchange concessions are at risk of being caught in a classic pincer movement. On the left flank is the reducing cash reliance which may well drive down lower strike rates and therefore turnover at airport concessions. And on the right flank is increasing price transparency driven by internet-based competition/disruption and internet-enabled price comparisons; both of which put pressure on margins and therefore a concessionaire’s ability to pay the same levels of rent as they have historically.

This pincer movement may not yet be affecting all airports or all airports in the same way. Airports with high demand for exotic currencies for example may be less susceptible to these forces, allowing them to continue to grow and achieve high margins which have historically flowed through into high rents. Nevertheless, these forces are long term and global trends which are likely to have a profound effect on airport currency exchange concessions.

Currency exchange operators have attempted to counter these forces and maintain business growth by selling ancillary products such as travel insurance and mobile phone SIM cards with, to date, mixed levels of success.

And then along comes COVID-19. Global firm Research and Markets has predicted that COVID-19 could push Australia to become Asia Pacific’s “first cashless society” by 2022, although the Commonwealth Bank (Australia’s largest bank) was more cautious, saying that was likelier to happen by 2026. Either way, the portents are not great for airport currency exchange concessions in the longer term, let alone taking into account the more immediate impacts of COVID-19 on currency exchange operators due to travel restrictions.

Cash is no longer king. While cash isn’t dead yet, and is unlikely to be killed off any time soon, the implications for airport currency exchange concessions are clear.

It is worth noting that one of the world’s leading currency exchange operators at airports, Travelex, recently appointed PwC as administrator citing – amongst other things – the impact of COVID-19 on its ability to trade and, after some restructuring, looks likely to emerge as a somewhat different business to its past form.

While airports will continue to have currency exchange concessions, any reduction in income from these concessions is not going to be easy to replace. Much of the currency exchange revenue in airports comes from locations such as kiosks in baggage halls or in arrivals halls – both of which have limited alternatives for income generation. The growth of arrivals convenience stores, mobile phone SIM cards sellers and F&B offerings are some ways in which airports have tried to counteract the potential for income loss from currency exchange.

Maybe it’s time to incorporate currency exchange services into other retail concessions like duty free or travel essentials? It’s not as far fetched as it might seem. In Australia, supermarkets have become the new ATMs with consumers able to withdraw up to A$400 from bank accounts or credit cards when paying for groceries by card. “Would you like cash with that?” is the new patter of supermarket checkout operators, borrowing and adapting McDonald’s highly successful “would you like fries with that” sales technique. So why not for duty free or travel essentials? It might be an interesting footfall driver for these outlets as well in the same way that domestic retailers and post offices become agents for services like Western Union.

Currency exchange operators also often perform other important functions at airports such as accepting local and foreign currency deposits from other airport retailers (e.g. duty free retailers) and tenants. These additional functions will also be hard for airports to replace and may drive up some operational costs for retailers (although this might be offset by lower cash counting and reconciliation costs). Currency exchange operators are also often the main providers of ATMs.

![]()

So while COVID-19 might be creating even stronger headwinds for airport currency exchange concessions, airports need to adapt to the challenges of still providing important currency exchange services to their passengers and replacing the rivers of cash that used to come from currency exchange.

Ivo Favotto contact: Tel: +61 423 564 057; E-mail: ifavotto@themercuriusgroup.com; Website: www.themercuriusgroup.com