AUSTRALIA/NEW ZEALAND. Ivo Favotto, a Sydney-based executive and company owner who has worked for all three stakeholders in the Trinity ecosystem, presents his latest commentary and figures on the gradual re-emergence of airport commercial activities in Australia and New Zealand.

AUSTRALIA/NEW ZEALAND. Ivo Favotto, a Sydney-based executive and company owner who has worked for all three stakeholders in the Trinity ecosystem, presents his latest commentary and figures on the gradual re-emergence of airport commercial activities in Australia and New Zealand.

Favotto owns and runs The Mercurius Group, a consultancy focused on industry research, consultancy and benchmarking studies, as well as operating his own destination merchandise supply business.

Here, Favotto – in the latest edition of his unique monthly report tracking the recovery of an initial 832 travel retail outlets across Australia and New Zealand – reflects on further setbacks to the pace of travel retail reopening in Australasian airports in the face of the latest COVID-19 developments.

He also provides an update on a case study which compares the fortunes of retail and F&B outlets in Manchester (UK) and Melbourne airports.

Have you ever been in a situation when you’re going one way and everybody else is going the other?

It’s an uncomfortable feeling. Either you know something that everyone else doesn’t know or they know something you don’t know. And even if you think you know something that everyone else doesn’t know, going the other way to everyone else is hard work and can fill you with self-doubt and anxiety.

That is precisely the situation that travel retail in Australia and New Zealand finds itself in right now.

Amid seemingly endless announcements after announcements of travel retail stores reopening coming from North America and Europe and countries such as the UK celebrating so-called Freedom Day, travel retail down under went backwards by more than six months in July.

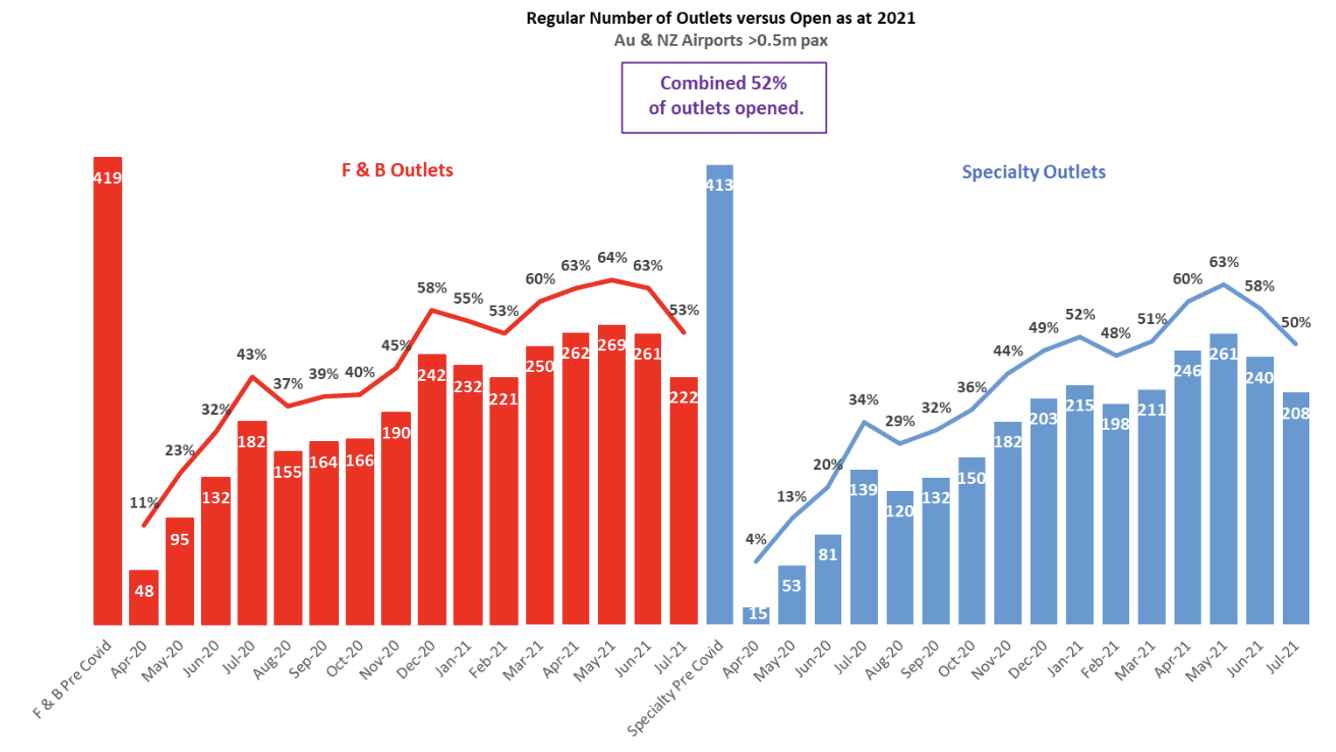

According to The Mercurius Group’s 16th monthly report tracking the recovery of travel retail in Australia and New Zealand from the COVID-19 pandemic, only 52% of travel retail stores were open in July 2021 compared to the number of stores open pre-pandemic in 2019.

The ratio of stores open has plunged from a high of 64% reported in May and takes travel retail back to the dark days of late 2020.

Why did this happen? Answer: Another COVID-19 outbreak in Sydney (Australia’s most populous city) and the reimposition of harsh lockdowns quickly extending from Sydney to other states as the outbreak spread. And, of course, the closure of the Trans-Tasman travel bubble between Australia and New Zealand for at least eight weeks.

In Australia and New Zealand, we are witnessing a Godzilla versus Kong style struggle to the death between the highly virulent Delta strain of COVID-19 and the Australia and New Zealand government’s island fortress mentality of shutting the doors and waiting for it all to go away. At this stage, we are not sure which is going to die first – the travel economy or the virus.

The (relatively) good news is that between two countries with a combined population of around 30 million, there have only been 947 COVID-19 deaths (97% of these were in Australia and just 3% in New Zealand). That’s small on a global scale where more than four million deaths have been recorded so far.

“As we are seeing in the UK, the longer the pandemic drags on and the bigger the economic cost, the more willing some become to pay the price of freedom”

But the financial cost is climbing exponentially the longer this pandemic and related fortress mentality continues. Adding to the sense of distress is that the burden is being felt unequally, with the travel and hospitality sectors (including travel retail) bearing a disproportionate load.

While both economies are awash with unprecedented levels of debt-fuelled corporate and personal welfare payments sending both stock prices and housing prices to new highs on an almost daily basis, the travel and hospitality sectors are suffering their longest and deepest recession in living memory, depleting both capital and human reserves and only just hanging on.

Across Australia and New Zealand airports, July saw total number of F&B outlets open drop to 53% (from a high of 64%) and total number of specialty outlets open drop to 50% (from a high of 63%).

The major contributor to the drop in stores open came from Sydney Airport where, in response to the state effectively being closed off to the rest of the country and New Zealand, several stores closed once again. The number of stores open at Sydney has figuratively fallen off a cliff, with only 17% of specialty stores and 16% of F&B sites open.

The rate of total store reopening is materially higher in New Zealand (74%) than in Australia (46%). New Zealand enjoys unrestricted domestic travel while the worst effects of the suspension of the international travel bubble with Australia are yet to be felt. And of course the rate of store reopening is higher in domestic terminals (82%) than international terminals (47%).

It is acknowledged that managing a country through a pandemic of this magnitude requires the almost unthinkable judgement about the economic value of a life. Open up too early and thousands more people may die of COVID-19. Open up too late and thousands more businesses (and people’s livelihoods which may in turn have serious health consequences) may die.

Tough choice. As we are seeing in the UK, the longer the pandemic drags on and the bigger the economic cost, the more willing some become to pay the price of freedom.

Hope springs eternal in the form of a vaccine programme. Once enough people get vaccinated, we’ll be able to return to normal, won’t we? Will we? I hope so. Right now you’d have to say that the jury is still out. And we may need to roll out a vaccine programme again and again. And then again, there may be new variants.

The reality is that we don’t really know. The eyes of the world are certainly on the ‘UK experiment’ where they declared 19 July as ‘Freedom Day’ while the virus remains rampant. At least vaccine rates in the UK are high. At time of writing, 44% of Australians and 55% of New Zealanders have had at least one jab while the proportion that have had both jabs sits below 20% in both countries.

Australian Prime Minister Scott Morrison recently announced that domestic lockdowns would stop after 70% of the population was double vaccinated and that international travel restrictions would be lifted once 80% of the population was double vaccinated. At this stage, this seems unlikely before year end.

Case Study update: The Tale of Two Cities – Melbourne and Manchester

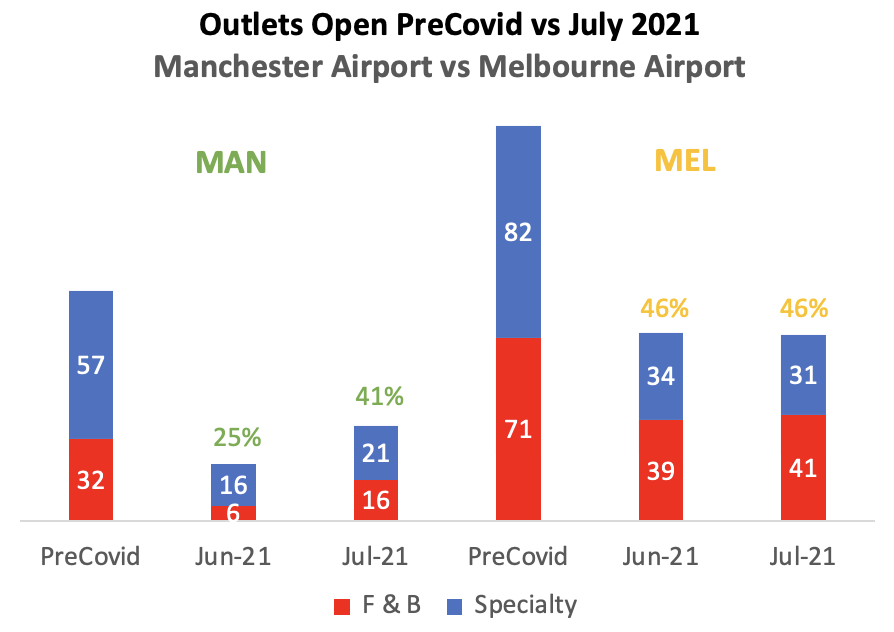

Last month, we reported on the different rates of travel retail reopenings at Melbourne Airport (Australia) versus Manchester Airport (UK). We found that the rate of store reopening was much higher in Melbourne than Manchester.

This month however, we report a significant narrowing of the gap. While the rate of reopening has remained stagnant at Melbourne Airport (46%), Manchester Airport’s travel retail programme has been buoyed by the reopening of its newly-transformed Terminal 2 which saw outlets open at the UK airport climb from 25% to 42% (50% in F&B and 28% in speciality).

The differences in travel retail recovery can be seen in the change of outlets open between our comparison between Manchester Airport and Melbourne Airport.

With the UK having established 19 July as Freedom Day and Melbourne Airport (again) caught up in the fresh wave of lockdowns gripping Australia, we fully expected the rate of reopening at Manchester Airport to overtake the rate of reopening at Melbourne Airport next month.

As Manchester Airport swims with the tide of travel retail reopenings sweeping across Europe and North America, Melbourne Airport, like most airports down under, seems to be swimming against the tide.

Footnote: The Mercurius Group, in partnership with The Moodie Davitt Report, has released the inaugural edition of the Airport Food & Beverage Study (AFABS).

The AFABS 2021 edition focuses on the Australian and New Zealand airport F&B markets, covering all 27 airports in Australia and New Zealand with annual passenger volumes exceeding 0.5 million.

The AFABS 2021 also features The Mercurius Group’s Top 12 F&B Operators League Table. These particular operators are responsible for 75% of the outlets within the region.

Other key features of AFABS Australia and New Zealand include:

- An estimate of overall airport F&B sales in the Australian and New Zealand market;

- F&B PSRs by country, terminal type and airport size;

- F&B PSRs by outlet type, outlet location and operator size;

- The number and type of F&B outlets in the market;

- A ranking of the Top 12 F&B operators by sales and a profile of their outlet portfolio; and

- A profile of the F&B programme for each airport (and for each terminal where applicable).

Other special features of the publication include a commentary on:

- How airports build an F&B programme; and

- The potential for F&B operator consolidation (mergers and acquisition activity) in the Australian and New Zealand airport F&B market.

To purchase a copy please contact The Mercurius Group:

Tel: +61 423 564 057;

Email: ifavotto@themercuriusgroup.com;

Website: www.themercuriusgroup.com