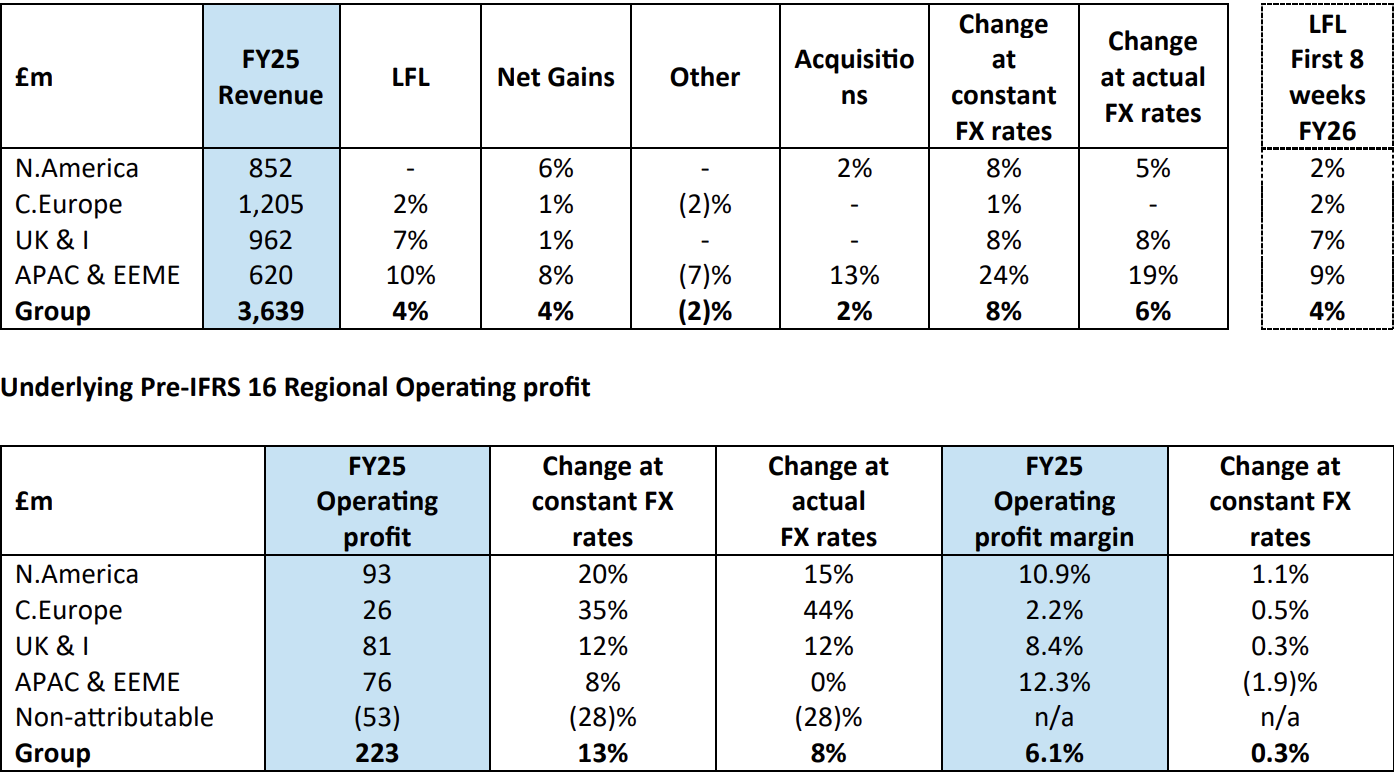

UK/INTERNATIONAL. Travel dining specialist SSP Group today (4 December) announced full-year results to 30 September, with revenue up +6% year-on-year (+8% at constant exchange rates) to £3.6 billion (US$4.8 billion).

Operating profit reached £223 million (US$297 million), up +8.3%, with EBITDA rising +6% to £364 million (US$485 million) and net profit climbing +19% to £95 million (US$126.7 million).

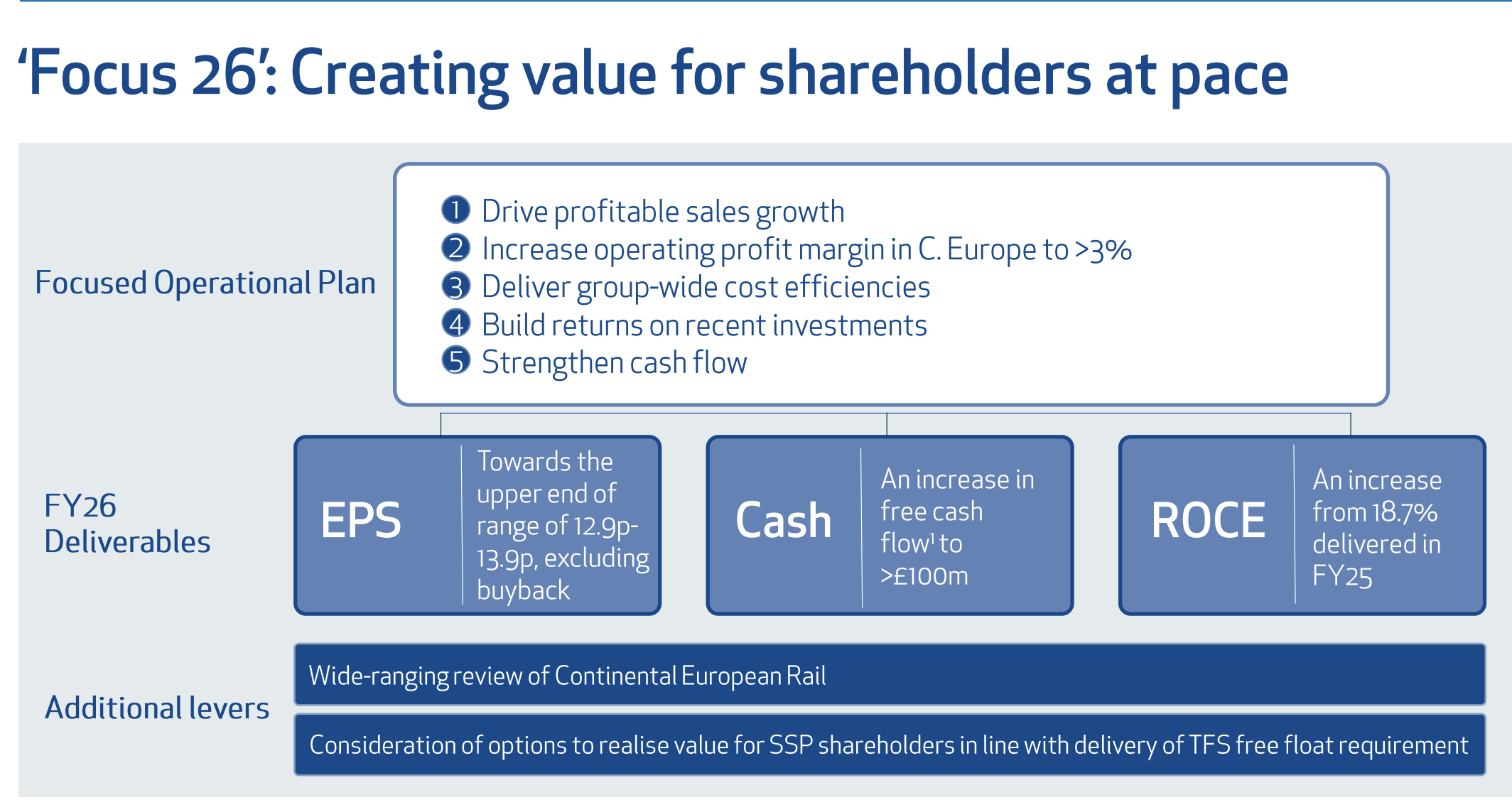

SSP said it was beginning a review of its Continental European rail business and looking at options “to realise value for SSP shareholders in line with the delivery of the Travel Food Services free float [India] requirement”. More details below.

Full-year revenue growth at constant rates included like-for-like growth of +3.7% and net new space growth of +4.1%, with the latter comprising 3.5% from organic net contract gains and 2.5% from acquisitions. A further -1.9% ‘other’ impact of new space growth was the previously announced staged exit of SSP’s German motorway services business and the reported loss of sales from its lounge business in Mumbai, with this now being accounted for as an associate and no longer consolidated in the results (see below).

SSP commented, “Against an unsettled macroeconomic backdrop and a softer demand environment in some of our key travel markets in the second half of the financial year, Group like-for-like sales growth of +4% in FY25 was in line with our guidance of c.4-5%.

“We focused on driving like-for-like sales through both increasing passenger conversion rates and average transaction values. Across all markets, we have innovated our customer and client offer, including with experience-led concepts such as Shelby & Co. at Birmingham Airport, Tigerstaden at Oslo Airport and Sky Gamerz at Seattle Airport in America. We also continued to roll out our digital ordering and payment systems, with 31% of our transactions now taking place on a digital ordering system.”

Since year-end, trading has gained momentum said SSP, with total revenue during the first eight weeks (from 1 October to 25 November) up +6% year-on-year on a constant currency basis. This includes like-for-like growth of +4%, up from +2% in H2 FY25, most notably driven by improved momentum in North America with like-for-like of +2% in the eight weeks.

CEO Patrick Coveney said, “We have delivered a resilient financial performance this year, with revenue and EPS up +8% and +25% respectively, on a constant currency basis, and a pivot to positive free cash flow.

“As a result of our actions in the year, including an ongoing focus on cost efficiency, we saw strong trading across three of our four regions. However, we acknowledge there is more to do to strengthen our operational performance, most notably in Continental Europe where we have now reset our team, model and balance sheet, and have a range of initiatives underway to do so.

“In addition, we are announcing today the launch of a wide-ranging review of our rail business in Continental Europe.

“While there remains a degree of macro-economic uncertainty across the world, our focus is on what we can control. We have made an encouraging start to FY26, with like-for-like sales growth now positive in all regions and tracking at +4% year-to-date for the group as a whole. This early momentum, together with the specific actions that we are taking to deliver sustained improvements in profit, cash and return on capital, gives us increasing confidence in our prospects for the coming year.”

Commenting on the plan to strengthen performance announced last December, SSP said it continued to drive profitable organic growth and contract retention, prioritising high growth and high returning markets, targeting mid-single-digit sales growth.

A revised recovery plan for Continental Europe includes increasing regional operating profit margin from 2.2% to over 3% in FY26, rising to around 5% in the medium-term.

A programme of cost efficiencies, including a recent corporate and regional overhead restructuring plan, will deliver an annualised saving of £30 million (US$40.1 million) (£5 million (US$6.7 million) in FY25 and the remainder in FY26).

The company also said it will build returns from recent investments and tighten new capital investment, with a further year-on-year reduction in capital investment from £212 million (US$282 million) in FY25 to no more than £200 million (US$267 million) in FY26, with “ongoing de-prioritisation of M&A”.

SSP noted that it had not delivered adequate returns on rail investments in Continental Europe. “Given this under-performance and in addition to the revised operating plan for Continental Europe, the Board has initiated a wide-ranging review of our Continental European rail business.” Supported by advisor Alvarez & Marsal, this will “consider and assess all potential options”, with a report due by May 2026.

On 14 July 2025, SSP listed Indian subsidiary Travel Food Services (TFS) on the Indian stock exchanges. As at end November 2025, TFS is trading at an equity value of around £1.5 billion (US$2 billion).

At the point of the TFS IPO, SSP’s partners and co-promoters K Hospitality sold down 13.8% of their shareholding to create an initial free float. Indian listing rules require a minimum free float of 25% of TFS shares within three years of listing. The SSP shareholding is currently 50.01%.

SSP said, “We continue to believe that India’s market potential, combined with TFS’s attractive economic model and market leadership, and a strong and balanced ongoing partnership between SSP and K Hospitality, offers a compelling opportunity for growth and returns for the group.

“As we work with our partner K Hospitality, to develop forward-looking plans for TFS, the board will explore options to realise value for SSP shareholders in line with the delivery of the TFS free float [India] requirement.”

Regional performance

In North America, full-year revenue of £852.3 million (US$1.13 billion) increased +8.3% on a constant currency basis, including a like-for-like decline of -0.4% and contributions from new space of +8.7%, including acquisitions of +1.9%. At actual exchange rates full year revenue increased +4.7%. Underlying operating profit for the period was £99.4 million (US$132 million), up +13.5%.

A statement noted, “In North America, where we experienced lower passenger numbers across our network of airports in the second half of FY25, we implemented a set of initiatives to drive like-for-like sales, such as incentivising units for the strongest sales delivery, enhancing technology and ordering systems, more consistent merchandising, revised menus and a particular focus on Sunday trading effectiveness.

“Through organic new wins, we continued to strengthen our position in the 56 airports in which we traded at the end of FY25 with incremental restaurants including at JFK Airport terminals 5 and 6 and Denver Airport.”

In UK & Ireland, full year revenues were £961.7 million (US$1.28 billion), representing a +7.8% increase on a constant currency basis, including like-for-like growth of 6.6% and contributions from net contract gains of 1.2%. At actual exchange rates full-year revenue also increased +7.8%.

On a pre-IFRS 16 basis, the region’s underlying operating profit was £81.2 million (US$108 million), up +12%.

In the UK, key activity included the rejuvenation of units at Newcastle, Liverpool, London City and Birmingham airports while SSP also won a new contract at Bournemouth Airport. Other actions to refresh and innovate the offer included the refurbishment of M&S retail units, including new layouts, merchandising, digital tills, lighting, signage and flooring.

Despite the impact of the M&S systems issues, following its cyber incident in the spring, SSP reported an average +10% sales uplift across these refurbished M&S stores in the year.

In Continental Europe full-year revenue of £1,204.5 million (US$1.6 billion) increased +0.5% on a constant currency basis, including like-for-like growth of 1.6% and a reduction from net contract losses of -1.1%, including -2% from the exit from German motorway services. At actual exchange rates full-year revenue decreased -0.2%. Underlying operating profit for the period was £42.4 million (US$56.5 million), up +8.4%.

In the APAC & EEME division, full year revenue of £620 million (US$827 million) increased +24.3% on a constant currency basis, including like-for-like growth of 9.7%, contributions from net contract gains of 7.7%, 13.5% from the acquisition of the ARE business in Australia and -6.6% from the transfer of the lounge business in Mumbai into a joint venture, Semolina Kitchens, now reported as an associate. At actual exchange rates full year revenue increased +19.4%.

SSP said it focused on building returns from the recent Airport Retail Enterprises acquisition in Australia and joint-venture investment with Taurus Gemilang in Indonesia, while building scale and profitability in more recent new country entries, such as Malaysia.

In India, the second-largest market in the region in sales terms, SSP secured two new contracts: 11 restaurants and a lounge at Cochin International Airport’s domestic terminal, and 14 restaurants at Delhi Indira Gandhi International Airport.

Additionally, SSP expects to commence new operations at the upcoming Noida and Navi Mumbai airports soon.

In Egypt, SSP extended contracts in three airports, to operate a total of 20 units.

Across the world, noted SSP, contract retention levels remained strong at more than 80%. Renewed contracts in the year include Leeds and Belfast International airports in the UK, Lanzarote Airport in Spain, Zurich Airport in Switzerland and Frankfurt Airport in Germany.

Selective growth

In an investor presentation today, SSP senior management noted that the company would be more “selective and challenging” on how it pursues new business.

Speaking later to The Moodie Davitt Report, Patrick Coveney said: “Publicly listed businesses in our sector are under pressure from investors on how they are spending capital, and the scale of capex step-up in 2023, 2024 and 2025 compared to pre-COVID was very marked, which was not surprising given all of the activity as the market played catch-up.

“But that level of capex step-up relative to cash flow, although needed in that period, was not sustainable.

“Industry-wide the pace of renewals has fallen off. For example in 2025 we renewed around 8% of contracts compared to the high teens in the first 18 months since I joined the company. So there has been a normalisation of renewals capex, but in turn that will allow us to be more cash-generative and to invest more in the longer term. And by the way, £200 million a year in capex going forward is not a small amount.”

Commenting further on the level of tenders and concession terms in the market today, Coveney said: “As a general trend across the world, and there are pockets of difference, but tenders are coming out where the length of contract is longer.

“Some markets place a much greater premium on pure commercial rent offers than others. In general, America places less of a focus on pure rent offers and more on other things. And a consequence of that is you end up with an average level of rent in America in the mid to high teens, versus the rest of the SSP estate, which would be in the mid-20s. And that is a point of difference.”

In the investor presentation, SSP senior management set out the rationale for a review of the rail business in Continental Europe.

Coveney said: “We are not delivering adequate returns on our rail business in Continental Europe. There are a range of drivers for this, including the slow post-COVID recovery in passenger numbers, changing passenger profiles, a marked increase in F&B space and competition across the rail network and reduced consumer spending levels in several of these markets.

“We have an operational plan to build margin in Europe to 5% but that is not enough. We need to do more to build the margin levels across our European business so given the level of issues in this channel and the necessity to assess all options objectively and at pace, we have appointed an external advisor, Alvarez & Marsal, to support us in the review. In this part of our business, the review has a wide ranging scope of potential options.”

Coveney would not be drawn on whether this could mean a disposal, but said that this option was complex given how some agreements in the channel are structured.

“Getting into too much speculation on what might or might not happen is probably unhelpful. But the nature of this kind of business, unlike many others, is that it doesn’t lend itself to easy divestment options. And so a lot of the focus on this work is incremental improvements that we can do, recognising that there may be things around the edges that we’ll look at in terms of ownership and participation.”

He added, “Very specifically though and we wouldn’t normally be drawn on this, is we are not in possession of any approach [for the rail business].

“You can assume that our board has educated itself on what the appetite might or may not be for an alternative strategy, and what that might or might not mean for the value that is available to us. And so having done all of that, we have landed on the plan that we shared today. You can take it that we will be responsible custodians of shareholders’ money, and will act accordingly.”

On the review of rail in Europe, he told us: “From an SSP viewpoint, we have become a company much more weighted towards the air channel. So when we review rail in Europe, we are saying we don’t want to invest further capital in a channel that delivers lower returns.

“One thing you will know is that we are very positive on European air, with big opportunities and renewals in key locations. In rail we need a review in light of our plan to structurally move margins forward.”

On maintaining the rate of revenue and profit growth in North America, Coveney said: “In the first two years I was here we went from around 30 North American airports to around 60. We are now moving towards an approach where we want to grow in locations we already have a presence.

“You can also see our EBIT margin has grown a lot, from 3.8% in FY22 to 11.1% in FY25. So to maintain that high level we will invest further in those profitable locations we are in.”