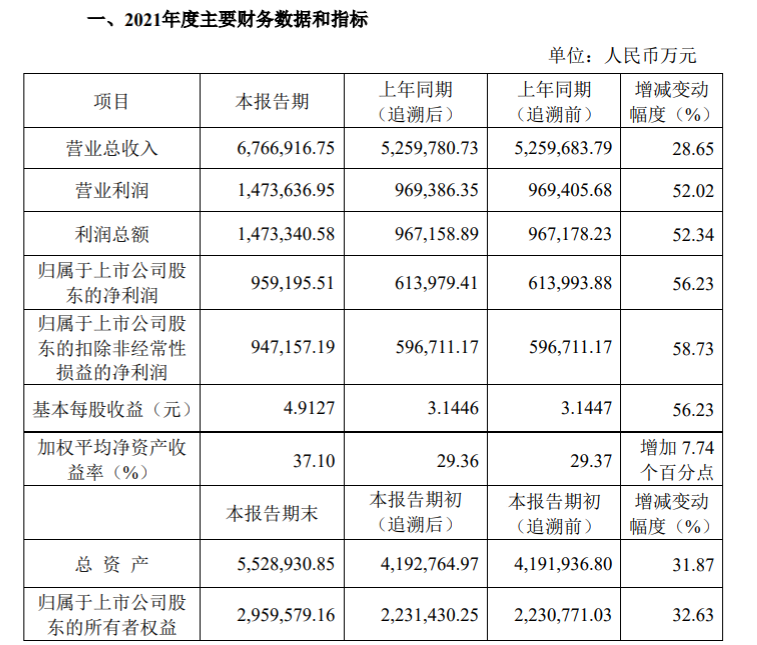

CHINA. China Tourism Group Duty Free (CTGDF) overcame difficult trading conditions caused by the COVID-19 pandemic to post a (preliminary) +52.02% year-on-year rise in 2021 earnings before tax to CNY14.736 billion (US$2.33 billion). Revenue rose by +28.65% to CNY67.7 billion (US$10.7 billion).

CTGDF, the parent company of China Duty Free Group (CDFG) – the world’s number one travel retailer by sales – achieved headline net profit of CNY9.592 billion (US$1.5 billion) an increase of +56.23%.

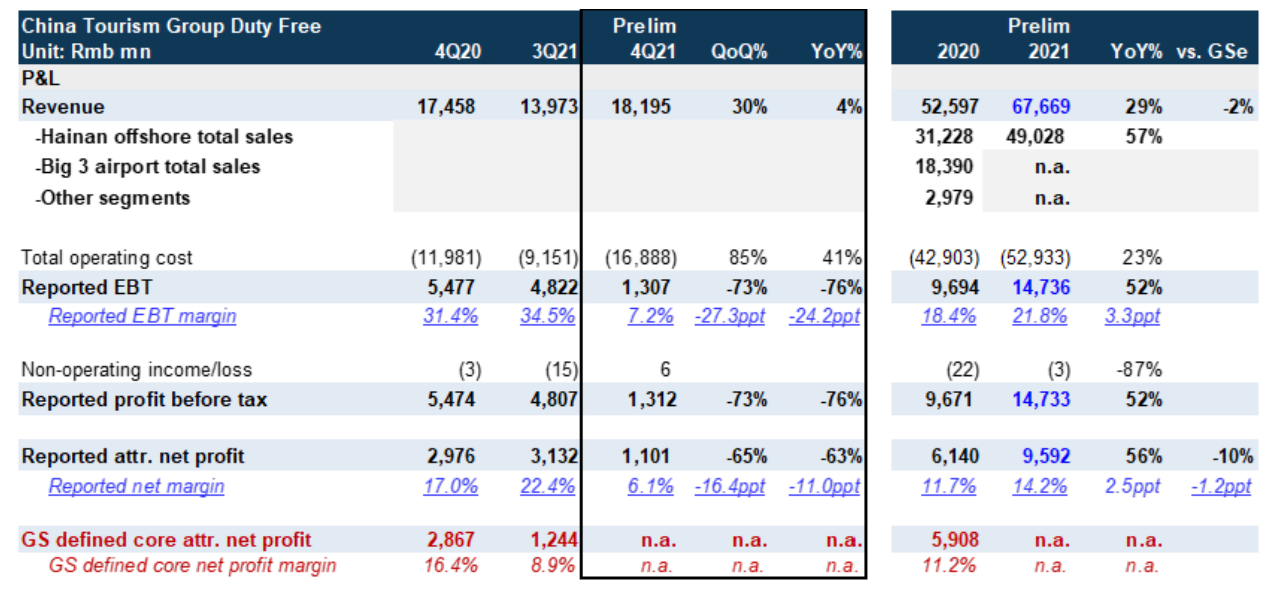

Group Q4 revenue rose +4% year-on-year (+30% quarter-on-quarter) to CNY18.2 billion (US$2.88 billion).

CDFG’s strong performance in the Hainan offshore duty free was the key driver. Sales in the island province rose +57.07% in 2021 to CNY49.03 billion (US$7.74 billion), the retailer revealed during a post-results call (see details below), a 72.45% share of group revenue.

Commenting on the robust results, CTGDF said: “This is mainly because the company focused on its core activity, the duty free business, and set strong foothold in the Hainan offshore duty free market to maintain high business growth.”

As reported, Hainan island’s offshore duty free stores generated sales of CNY60.17 billion (US$9.47 billion) in 2021, an +84% increase year-on-year.

Improved contract terms (already in place at Shanghai Pudong Airport) also helped. “After equal, friendly consultations, a subsidiary of the company has reached an agreement with Beijing Capital International Airport regarding lease concessions in the third contract year and has signed a supplementary agreement,” CTGDF said.

In a note Goldman Sachs pointed out that the strong Hainan sales recovery (+54% quarter-on-quarter in Q4) was propelled by ongoing pricing discounts and promotional activities, which dented profit margins.

However, based on a China Tourism Group post-results call with analysts and investors on Friday 21 January, Goldman Sachs said that CDFG’s 2022 strategy in Hainan is to focus on profitability by scaling back promotional activities and “irrational” competition (in consensus with fellow Hainan duty free retailers). “Indeed, our channel checks suggest lower pricing discounts in Hainan recently,” the report noted.

Korean daigou crackdown?

In another important take-out, Goldman Sachs said that CTGDF still sees considerable scope for growth in Hainan given the upside across various parameters such as shopper conversion ratio and per-shopper spending.

It commented: “When international borders re-open, CTGDF will inevitably be affected given the dilution of spending into overseas countries. But the company is hopeful to make up any such dilution by sale resumptions at airport/downtown duty-free stores.”

Importantly, Goldman Sachs said that CTGDF management believe that the Chinese government will scrutinise Korean daigou activity into China more closely and impose tighter restrictions, thus boosting spending within China. The report noted that China’s duty free market was worth around CNY80 billion (US$12.6 billion) last year, still below South Korea’s approximate US$15.8 billion channel.

That was despite strict travel restrictions remaining in place in the Republic with no inbound Chinese visitors (as a result South Korea’s duty free market remains overwhelmingly reliant on daigou trading, with foreigners accounting for some 94% of sales -Ed), Goldman Sachs noted.

Margin improvement likely

CTGDF told investors and analysts on Friday that 2022 will see a shift in focus to profitability over revenue scale. “As opposed to benchmarking with Korea operators which generate merely single digit % margins, CTGDF believes it can bring its gross margin closer to Dufry’s 55-60% level, leveraging on its business scale and product variety,” Goldman Sachs said.

This, balanced with a more restrained pricing approach across the island by all retailers, should boost margins through 2022.

CTGDF will also work hard to improve store penetration and average transaction values to complement an already high (circa ~40%) shopper conversion rate, the group revealed.

Flexibility to extend contracts

Goldman Sachs noted that the Ministry of Finance issued a notice on 19 January giving airports or other channels the flexibility to extend duty free retailers’ contracts (separate story coming soon). With relief measures in place already at Shanghai Pudong, Beijing Capital International and Hong Kong International airports, CDFG stands to benefit from longer concession terms to generate profit in normalised years to compensate for the COVID-19 impact.