INTERNATIONAL. Alcohol volumes worldwide (across all channels) reached 27.6 billion nine-litre cases in 2018, a decrease of -1.6% from the year prior, according to new data from industry intelligence source IWSR. The research company however forecasts that consumption will steadily increase over the next five years, reaching 28.5 billion cases in 2023 (up 3% over the period).

In terms of retail value, the global market for beverage alcohol in 2018 was just over US$1 trillion, a number which the IWSR expects to grow 7% by 2023 as consumers continue to trade up to higher-quality products.

The figures are included in the just-released IWSR Drinks Market Analysis Global Database. A more detailed study of spirits’ performance in travel retail will appear later in the year.

![]()

HIGHLIGHTS

Gin led category growth in 2018, should reach 88 million cases by 2023

The largest gain in global beverage alcohol consumption in 2018 was in the gin category, which posted total growth of 8.3% versus 2017. Pink gin was a key growth driver, helping the category sell more than 72 million nine- litre cases globally last year.

In the UK alone, gin was up 32.5% in 2018, and the Philippines (the world’s largest gin market) posted growth of 8%, fuelled by a booming cocktail scene and premiumisation of the market, said IWSR. By 2023, the gin category is expected to reach 88.4 million cases globally, with particularly strong growth in key markets such as the UK, Philippines, South Africa, Brazil, Uganda, Germany, Australia, Italy, Canada and France.

Notably, Brazil has emerged as a hotspot for the category, with volumes there more than doubling last year and forecasted to grow at 27.5% (CAGR 2018-2023), as the gin-and-tonic trend has increased in upmarket bars of São Paulo and Rio de Janeiro.

Consumption of whisky and agave-based spirits increases

Spurred by innovation in whisky cocktails and highballs, the global whisky category increased by 7% last year, driven in large part by a strong Indian economy (whisky grew by 10.5% in India, as consumers continue to trade up in the category). The US and Japan posted 5% and 8% growth, respectively.

The IWSR forecasts whisky to grow by 5.7% CAGR from 2018 to 2023, to almost 581 million nine-litre cases. Also, continued interest in tequila and mezcal (especially in the US), and innovation in more premium variants and cocktails, drove the agave- based spirits category to 5.5% global growth in 2018 – and is expected to post 4% growth over the next five years (2018-2023 CAGR).

Mixed drinks and cider grow

The mixed drinks category (which includes premixed cocktails, long drinks, and flavoured alcoholic beverages) grew 5% globally in 2018. By 2023, it is projected that more than 597 million nine-litre cases of mixed drinks will be consumed across the world.

The growth is backed by continued strong gains in ready-to-drink (RTD) cans in the US and Japan, the category’s two largest markets. In Japan, most RTDs are locally made and almost exclusive to Japan. Their popularity is partly due to the fact that they are relatively dry, which makes them more food- friendly and sessionable, noted IWSR.

In the US, the popularity of alcohol seltzers has been an engine for growth in the RTD market. In the cider category, as investment levels in those products continue to rise, almost 270 million cases are expected by 2023, a 2.0% CAGR 2018-2023. Both of those categories (mixed drinks and cider) are taking share from beer as perceived accessibility increases (less bitter, easier to drink.)

Vodka, liqueurs, and cane spirits decline

Vodka lost volume in 2018 (-2.6%) as the market for lower-priced brands continued its decline in Russia and Ukraine (two of the largest markets for this spirit). Higher-priced vodkas, however, showed a more positive trend last year.

Nonetheless, noted IWSR, the outlook for total vodka over the next five years remains sluggish as the category is forecast to dip 1.7% (CAGR 2018-2023). Also in decline is the flavoured spirits category (liqueurs), which dropped by 1.5% globally in 2018, and is expected to continue to slip in 2019 before rebounding slightly in 2020. Cane spirits (primarily Brazilian cachaça) was down 1.6% last year, and is forecast to lose another 4.5 million cases by 2023.

Beer loses volume in 2018, but should rebound

Global beer sales declined 2.2% in 2018, hit from volume decreases in China (down 13%). Other large markets such as the US and Brazil also fell (1.6% and 2.3%, respectively), while Mexico and Germany saw growth (6.6% and 1%, respectively). The future outlook for beer, however, paints a more positive picture, as the category is expected to show a slight increase in 2019 and post 0.7% average growth through to 2023.

Wine volume declines, but value increases

Wine, which had posted strong global growth in 2017, lost 1.6% in volume in 2018 as wine consumption declined in major markets such as China, Italy, France, Germany and Spain (the US market was flat). However, though consumers are drinking less wine, they are increasingly drinking better – pushing wine value to increase, said the IWSR report. Globally, the retail value of wine is projected at US$224.5 billion by 2023, up from US$215.8 billion in 2018. The one bright spot in wine volume is the sparkling wine category, which is expected to show a five-year CAGR of 1.17% from 2018 to 2023, driven in large part by prosecco.

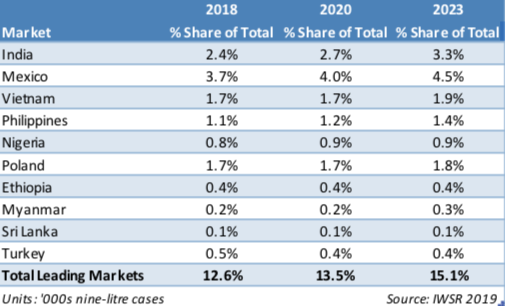

Top ten markets, 2018-2023

A look at the world’s fastest-growing beverage alcohol markets shows an emergence across a variety of developing countries, said IWSR. A combination of growing legal-drinking-age populations and healthy economies is driving some of this growth, which is expected to continue over the next five years.

“Every year our analysts spend months traveling the world to speak with suppliers, wholesalers, retailers, and other beverage alcohol professionals to assess what is happening market by market in this fast-changing business,” said ISWR CEO Mark Meek. “The raw data we collect is enormously valuable, but equally important is what that data tells us in terms of trends, challenges and opportunities facing the industry.”