INTERNATIONAL. Dufry this morning laid bare the drastic impact of the COVID-19 crisis on its business, revealing in a trading update to its first-quarter results that sales had plummeted -94.1% year-on-year in April. However, it also unveiled a coherent plan, driven out of crisis, to shore up liquidity and to drive recovery on a location-by-location basis as the situation improves.

The startling fall in April turnover, driven by the combined impact of closed national borders; near or total shutdowns of many airline and airport passenger operations, underlines the extent of the challenge faced not only by the giant of travel retail but also the sector as a whole.

The April trading update was contained in today’s announcement of first-quarter results, which were as expected a tale of three sharply contrasting months.

Dufry’s turnover reached CHF1,438.7 million (US$1,479 million) in the first quarter of 2020, a -20.8% decline in constant FX year-on-year (organic -21.4%). Performance during the period was significantly impacted by an “unprecedented” reduction in passengers flows in airports, cruise lines and touristic destinations around the world due to the spread of the COVID-19 crisis, Dufry noted. In the first quarter 2020, organic growth amounted to -21.4%.

A tale of three contrasting months

Dufry started the year positively, posting organic growth of +0.8% in January. In February, however, it started to see a gradual slowdown (especially in Asia), with organic growth falling to a negative -2.3% in the year. In March, many countries started to implement travel restrictions, partially leading to airport closures and a further deterioration of sales, which slumped -55.9% year-on-year.

In a trading update and outlook, Dufry said: “As expected, the business environment remained tough during April, with travel restrictions in place in most locations. Thus, sales stood at -94.1% in April periodic. Giving the current context, and the low visibility to provide business forecasts, the company has withdrawn the full-year 2020 guidance previously disclosed on March 12, 2020.”

In a trading update and outlook, Dufry said: “As expected, the business environment remained tough during April, with travel restrictions in place in most locations. Thus, sales stood at -94.1% in April periodic. Giving the current context, and the low visibility to provide business forecasts, the company has withdrawn the full-year 2020 guidance previously disclosed on March 12, 2020.”

Dufry Group CEO Julián Díaz commented: “At the beginning of 2020, we first saw an acceleration of the business and an encouraging performance. Then the crisis started to impact the travel retail industry and our performance in several locations as of February, leading to a negative performance for the first quarter of 2020.

“We have immediately set up a special committee, which has developed and implemented a comprehensive action plan focused on driving sales, secure cash generation, reduce costs and safeguard our profitability. The action plan has adapted the company’s structure to the current environment and considers different scenarios of full-year sales declines ranging from -40% to -70% and allowing us to flexibly adapt the measures to the business performance.

“Looking forward, Dufry has already developed a recovery plan on a location-by-location basis and is ready to resume operations as soon as travel restrictions are lifted. The recovery plan is based on each location’s productivity and includes a whole set of global initiatives to drive sales through promotions and adapting the assortment focusing on new products and exclusivities.

“Furthermore, in April, we successfully implemented several financial initiatives to strengthen our capital structure and improve our liquidity position. This is an important step and together with our cost-cutting initiatives, it will allow us to continue operations until the next cash generation cycle starts.

“Despite the currently challenging environment, we are strongly convinced that the business will recover as we have seen in previous occasions and we are well prepared to serve customers as soon as circumstances allow.”

Performance analysis

In the first quarter, organic growth was -21.4%, mainly impacted at like-for-like performance level due to lower passenger traffic across the majority of airports. All divisions reported negative organic growth, in particular Asia Pacific and the Middle East, followed by Europe & Africa; while North, Central and South America were influenced as of March.

Changes in scope, which includes the positive contribution of the acquisitions of Vnukovo [Regstaer operations -Ed] and Brookstone (the US bookstore chain acquired by Dufry subsidiary Hudson Group in 2019], amounted to 0.6%. The translational FX effect in the period was -2.8%, driven by the strengthening of the Swiss Franc versus the main currencies.

Reduced capex

With respect to business development, Dufry slowed down its refurbishment programme to reduce Capex. Nevertheless, shops in London, Athens, Macau, Los Angeles, and Guayaquil were renewed. The company also continued expanding its operations, with most space increases executed during January and the first weeks of February. Dufry opened new and expanded shops across several locations, including Helsinki, Perth, Indianapolis, Calgary, and Florianopolis, in the South of Brazil.

Action plan created with further initiatives in place

Dufry immediately defined an action plan and implemented operational initiatives at the end of January to drive sales, secure cash flow generation, save costs and safeguard liquidity.

The retailer said that it has further expanded its initiatives and adapted its operating structure to reflect the current business environment and to maximise leverage as from a traditionally flexible cost structure “even beyond the levels possible under normal conditions”. Dufry has based the action plan on different scenarios with FY sales declines ranging from -40% to -70%, with inbuilt flexibility.

The main initiatives taken are:

- Maintain level of gross profit margin in collaboration with brands

- Renegotiate agreements with landlords to reduce rents and concessions

- Personnel expense efficiency programme implemented, reducing costs at all levels, and making use of government support schemes whenever possible as well as implementing voluntary salary reduction schemes

- Reducing all operating expenses as much as possible and monitoring payments at Group level with a dedicated team

At a cash flow level, Dufry also implemented several measures to reduce cash outflows to a minimum. These are controlled tightly by a dedicated team at Group level. These initiatives include actions at Capex and Net Working Capital level with expected cash savings of around CHF160 million (US$165 million) in the full-year 2020.

Strengthened financial structure

As reported, in April Dufry announced a set of initiatives to strengthen its capital structure and liquidity position, designed to support the company in sustaining a prolonged period of significant disruptions and reinforce its competitive positioning in the longer term.

Those measures included:

- A new 12-month committed credit facility of CHF425 million with two 6-month extensions, subject to final documentation

- Successful placement of 5.5 million shares out of existing authorised capital generating gross proceeds of CHF151.3 million

- New convertible bond, which due to the strong demand, had its nominal amount of the issuance increased by CHF50 million to a total size of CHF350 million

- Signed agreement with banks to waive the existing financial covenants until end of June 2021 and a higher leverage covenant for the September and December 2021 testing periods

- Cancellation of the 2020 dividend, thus reducing short-term cash outflows

In addition, Dufry’s Board of Directors proposes to the upcoming Ordinary General Meeting on 18 May, the creation of additional conditional share capital sufficient to enable the physical settlement of the new convertible bonds.

In total, the new financing initiatives will improve Dufry’s liquidity position from CHF685.9 million (US$705 million) as of 31 March to a pro-forma position of CHF1,612 million (US$1,657 million).

Regional division performance (see charts below)

Regional division performance (see charts below)

Europe and Africa

Turnover in the Europe and Africa region was CHF534.8 million (US$550 million) in the first three months, with organic growth down -20.3%.

Performance was negative across most locations in the division, and particularly in Italy, Switzerland, UK and Spain with negative double-digit growth. Turkey posted a positive performance in the quarter supported by a good passenger traffic in January and February, but declining significantly in March. Performance in Africa was stable, with the growth in the first two months of the year being offset by the performance in March.

Asia Pacific and Middle East

Turnover amounted to CHF213.2 million (US$219 million), with organic growth down -30.2% in the worst affected division during the period.

North America

Turnover reached CHF330.2 million (US$340 million) in Q1 (organic growth -24%) in the period with duty free hit harder than duty paid sales due to its exposure to international and Chinese customers in particular.

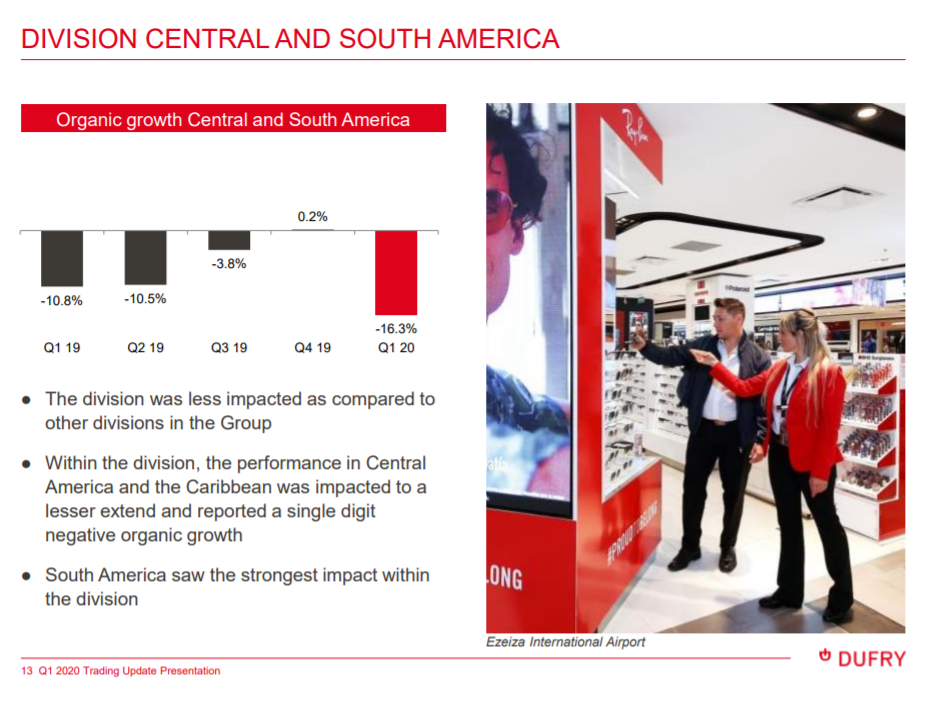

Central and South America

Turnover was CHF314.0 million (US$323 million) in the first quarter (organic growth -16.3%) The division was the least impacted of all within the group – in particular Central America and the Caribbean – as most travel restrictions took effect from March.