CHINA. China Duty Free Group (CDFG) parent company China Tourism Group Duty Free (China Tourism Group) unveiled robust preliminary H1 results last night, revealing a +484% rise in core net profit to RMB5.34 billion (US$826.5 million) from a low, COVID-affected 2020 comparative base.

First-half sales rose +84% year-on-year to RMB35,501 million (US$5.5 billion). Q1 sales reached RMB18,134 million (US$2.8 billion), easing -4% to RMB17,368 million (US$2.7 billion) in Q2. First half sales are likely to represent approximately 41% of 2021 revenue, according to Goldman Sachs.

The performance was driven by a continued strong showing in Hainan province where, as reported, total combined duty free and duty paid sales in the first half (all retailers) reached RMB27,383 million (around US$4.24 billion) according to Goldman Sachs – an increase of over +265% year-on-year.

The investment bank and financial services company estimated CDFG’s share of the Hainan market at 95% in Q1 and (thanks to retailer proliferation) 91% in Q2 (see below for details).

Goldman Sachs said the China Tourism Group results were in line with its expectations.

Its key takeaways included:

- Revenue -4% quarter-on-quarter: Attributable to seasonally weaker Hainan sales in June (Goldman Sachs projects RMB2 billion/US$650 million for Hainan duty free/duty paid sales in the month)

- A slower daily run-rate in June: RMB141 million/US$21.8 million (vs. RMB173-187 million in February-May) driven by weaker seasonality and flight cancellations from Guangdong due to a brief resurgence of new COVID-19 cases in late May.

- Traffic easing: The number of shoppers also dropped from 32.7k each day in May to 27.9k in June.

- CDFG market share holding strong despite proliferation of retailers: 91% market share in Q2 vs. 95% in Q1 with Hainan Tourism Investment capturing circa 6%, Hainan Development Holdings around 2% and CNSC 1-2% [with Shenzhen Duty Free/DFS accounting for the balance -Ed]

- Steady profit margin despite ongoing competition in Hainan: Earnings before tax amounted to RMB4.15 billion (US$642.4 million) vs. RMB4.46 billion in 1Q21 implying a relatively stable pre-tax profit margin of 23.9% (vs. 24.6% in Q1 21).

Goldman Sachs opined that although some of the new Hainan duty free retailers are offering attractive discounts of up to 20-30% on volume purchases, they are suffering from limited assortments compared with CDFG, a disadvantage that may be gradually diminished in future.

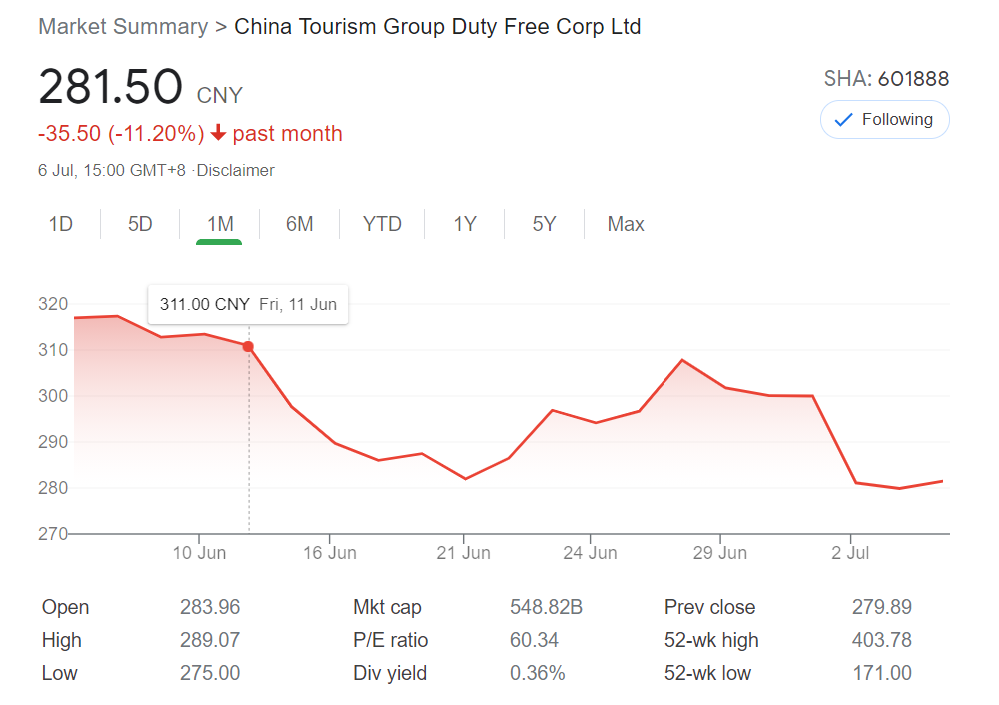

While China Tourism Group’s share price has eased by almost -12% over the past month, along with other travel-related stocks due to the Guangdong cases, the subsequent recovery there (no locally transmitted cases since 25 June) should spur the stock on the back of rising momentum as the key October to April trading period nears, Goldman Sachs noted.