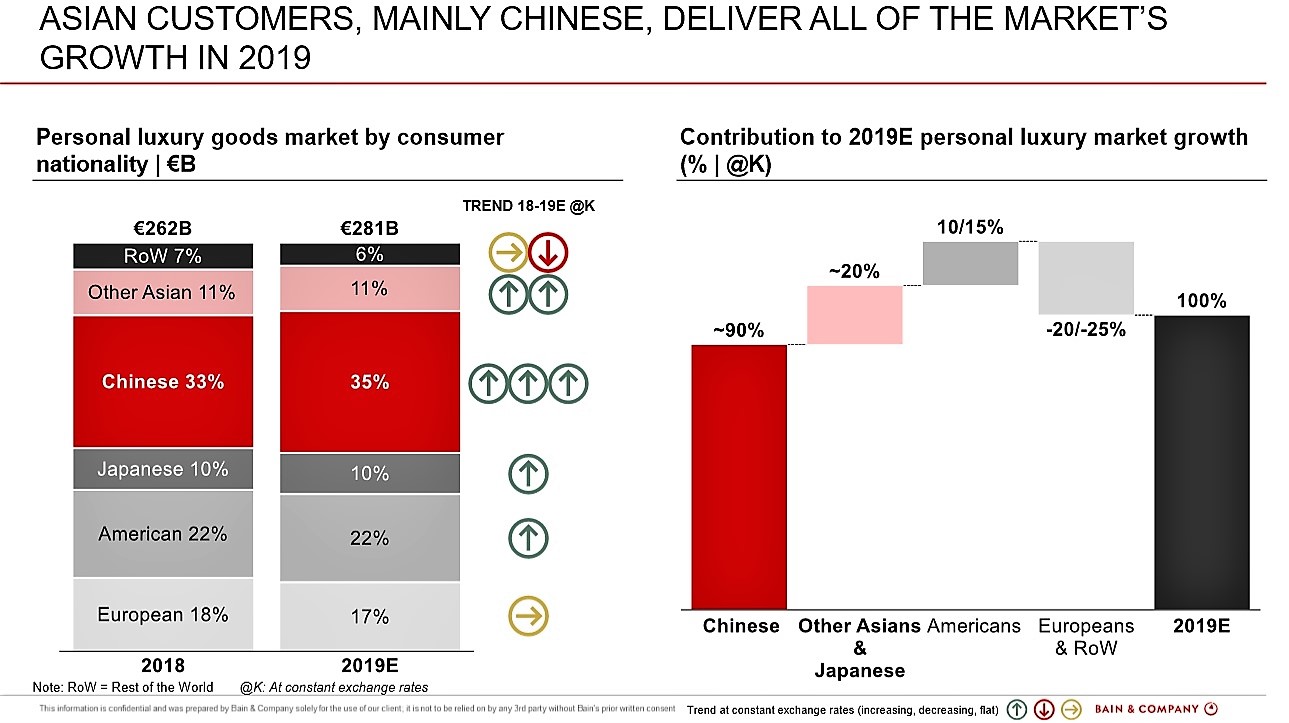

INTERNATIONAL.The Chinese – and other Asia Pacific nationals – were almost entirely responsible for the growth of the personal luxury goods market in 2019. That’s according to the 18th edition of the Bain & Company Worldwide Luxury Study, released in collaboration with Fondazione Altagamma, the Italian luxury goods manufacturers group.

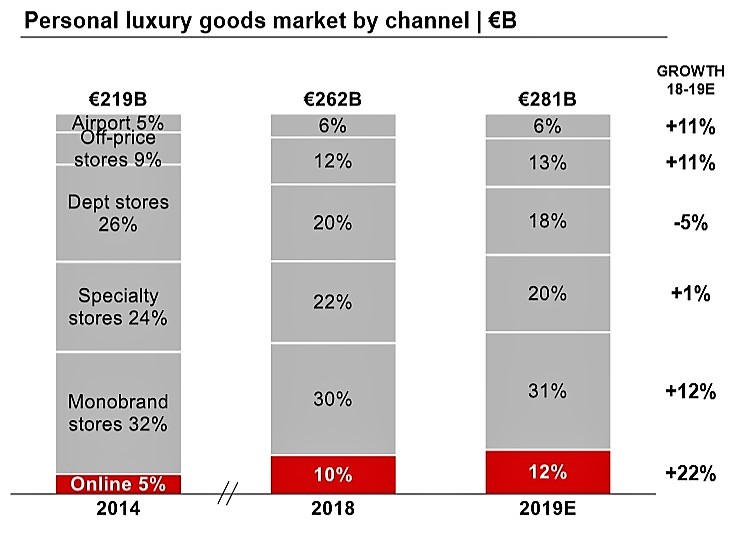

The airport and off-price channels also grew their combined share of the market considerably from 14% to 19% in the five-year period from 2014-2019 as tourist flows increased.

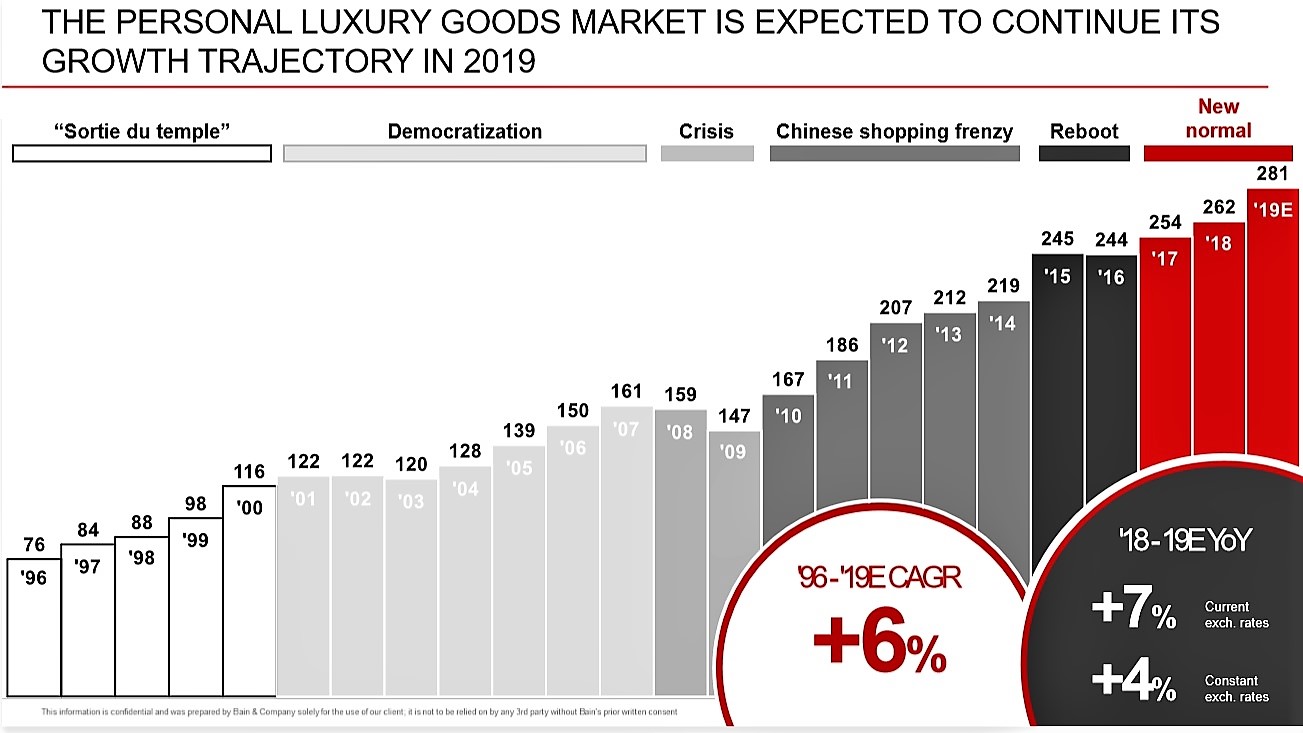

The in-depth report from management consultancy Bain & Company – written by Bain Partners Claudia D’Arpizio (lead author) and Federica Levato – indicates that the personal luxury goods market will have grown by +4%* (at constant exchange rates) and +7% (at current rates) to €281 billion by the end of the year. The increase amounts to an extra €19 billion.

“The global luxury market confirmed this year the moderate growth rate associated with the ‘new normal’ era (which is) mainly driven by Asian buyers,” said Claudia D’Arpizio.

Bain estimates that the Chinese contributed about 90% to personal luxury goods growth this year, with other Asians/Japanese adding another 20%. Americans added a further 10-15% but Europeans and Rest of the World (ROW) produced a negative drag of 20-25% to end the year at +4% overall.

The Chinese will have increased their share of global luxury sales to 35% in 2019 (from 33% last year); Europeans and ROW will both drop one percentage point to 17% and 6% respectively; and Americans, Japanese and Other Asians will hold steady on 22%, 10% and 11% respectively.

In terms of spends by location, Mainland China grew by +26% to €30 billion as luxury purchasing boomed. The Bain-Altagamma Worldwide Luxury Market Monitor put this down to “resounding local spending sustained by governmental policies and a shift in Chinese consumer flows repatriating from abroad” including from Hong Kong where social unrest is heavily influencing tourist flows elsewhere.

Japan was solid at +4% to reach €24 billion thanks to continuing tourist consumption. This was aided by Chinese consumers looking for alternatives to Hong Kong although “department stores were playing a lesser role in the channels’ ecosystems” according to the report.

Asia’s +6% increase to €42 billion was helped by a dynamic South Korean market “with robust local consumption strongly driven by young customers” stated D’Arpizio and Levato. Brisk growth in other Asian countries included Singapore, Thailand and Taiwan. Chinese tourist consumption surged across Asia, particularly following the unrest in Hong Kong.

Personal luxury spending in the three markets of Mainland China, Other Asia and Japan will contribute €96 billion of the year-end estimate of €281 billion.

Western markets remain dominant for luxury spending but Chinese and Asian spending there has been mixed. Growth in the Americas was flat (at constant currency) to reach €84 billion. The strong US dollar and the China/US trade war negatively impacted tourist consumption while Canada was affected by a contraction in Chinese tourist affluence.

In Europe – up by +1% to €88 billion – results by country varied, but weak currencies versus the US dollar positively impacted tourist spending. ROW, led by the Middle East, was flat due to lower local consumer confidence.

Airport/off-price and online take more share

Airport and off-price channels have expanded as their role becomes more crucial in leveraging larger consumer bases– tourists as well as mid-low spenders. Both channels accounted for an estimated 19% of the personal luxury market in 2019, up from 14% in 2014.

The only other channel to have grown in this five-year period was online – from 5% to 12%, helped by the fact that omnichannel environments remain a top priority for luxury players. Accessories and beauty maintain the lion’s share of growth, being easier categories to manage online.

Other core channels – department stores, speciality stores and monobrand stores – all saw their shares contract.

“The Hong Kong luxury landscape will be profoundly reshaped, with physical networks strongly re-dimensioned and rules of the game deeply transformed. ‘Local customers’ are the new name of the game” –Bain & Company Worldwide Luxury Study

Despite the airport momentum, there has been a general shift towards local rather that tourist spending in core regions. This could impact the duty free channel going forwards.

In Europe, there were mixed effects of tourism with “the Chinese demonstrating slowing dynamism and lower average spending” said Bain. Americans were back strongly, the Russians to some degree also; while Middle Eastern customers continued to yoyo.

In the Americas, a strong US economy drove up confidence – and local spending – while the high US dollar and the US-China trade war impacted tourism, especially to the US West Coast where high-end airport retailers rely on Chinese travellers.

Government policies and lower price differentials in Mainland China continued to fuel local consumption, as did political situations across the globe which hit Chinese spending abroad and drove am increasing preference to spend locally.

Hong Kong woes suggest a fundamental reshaping

With Hong Kong still mired in socio-political unrest, affecting the entire economy as well as the personal luxury market, the Special Administrative Region’s approximately 1,000 luxury monobrand stores are feeling some chill winds.

Luxury downtown travel retail giant DFS Group has taken a big hit, and there are no indicators yet of a tourism bounceback. “The Hong Kong luxury landscape will be profoundly reshaped, with physical networks strongly re-dimensioned and rules of the game deeply transformed. ‘Local customers’ are the new name of the game,” said D’Arpizio and Levato.

€375 billion by 2025?

Looking ahead, Bain is predicting that global personal luxury goods sales will grow by between +3% and +5% annually by 2025, valuing the market at €335-375 billion.

The consultancy believes that solid mid-term macro fundamentals such as rising numbers of middle class shoppers and a positive attitude towards buying luxury goods will pave the way for growth. However, D’Arpizio warned that there were possible bumps along the road – such as socio-political issues, government commercial policies and a possible short-term soft recession – “which could make the path less smooth”.

The surge will be helped by an enlarging luxury customer base – from the bottom up. This base will grow from 390 million in 2019 to 450 million by 2025, led by a wave of predominantly Asian middle-class consumers that will force structural changes for brands.

One of the changes, said Bain, will be stretching the product offer downwards towards entry-price items to cater to a large increase in new and aspiring luxury consumers – of whom at least 50% will be younger Generation Y shoppers. This trend could also boost downtown and/or arrivals duty free shopping in markets such as China and Japan as searches for the best prices for luxury brands increase.

* All growth percentages at constant exchange rates unless stated.