Anticipated pressures in the company’s Asia travel retail business and “incremental headwinds” from a slower-than-expected recovery of prestige beauty in Mainland China drove an -11% year-on-year decline in global organic sales (-10% net sales) at The Estée Lauder Companies (ELC) for its first quarter ended 30 September.

“We delivered our outlook for organic sales and exceeded the expectation for adjusted diluted EPS. Organic sales decreased -11%,” said The Estée Lauder Companies President and Chief Executive Officer Fabrizio Freda during an earnings call. “Our global travel retail business drove the decline, as expected, with organic sales lower by -51% given the combination of trade inventory reduction and a structured market containment.”

The sharp decline in global travel retail net sales was primarily due to the company’s and its retailers’ actions to reset key Asian retailer’s inventory levels [mainly in Hainan and South Korea]. The decrease also reflected changes in government and retailer policies related to “unstructured market activity” [a reference to the crackdown on daigou activity out of the same two key North Asian markets]. These actions and changes led to lower product shipments compared to the prior year, ELC said.

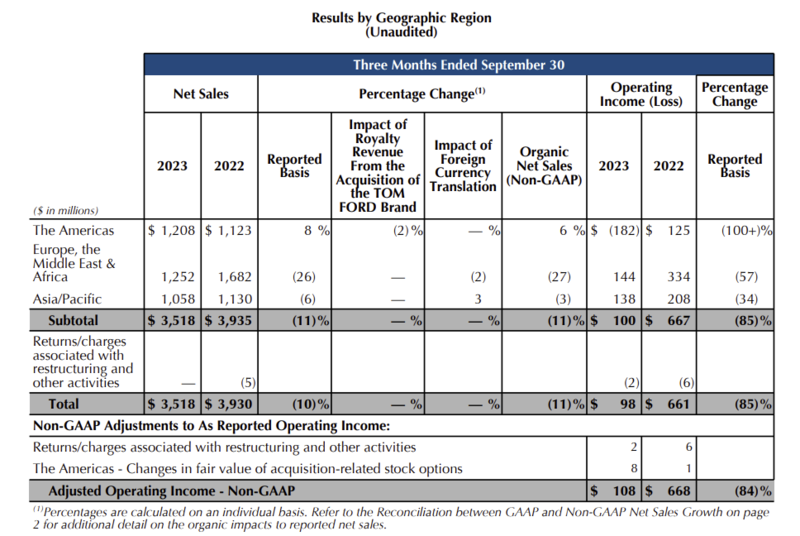

The US beauty powerhouse noted these challenges were partially offset by organic net sales growth in the US and many markets in Asia Pacific, led by Hong Kong SAR and Japan; as well as across nearly all markets in Europe, the Middle East & Africa (led by the UK) and Germany.

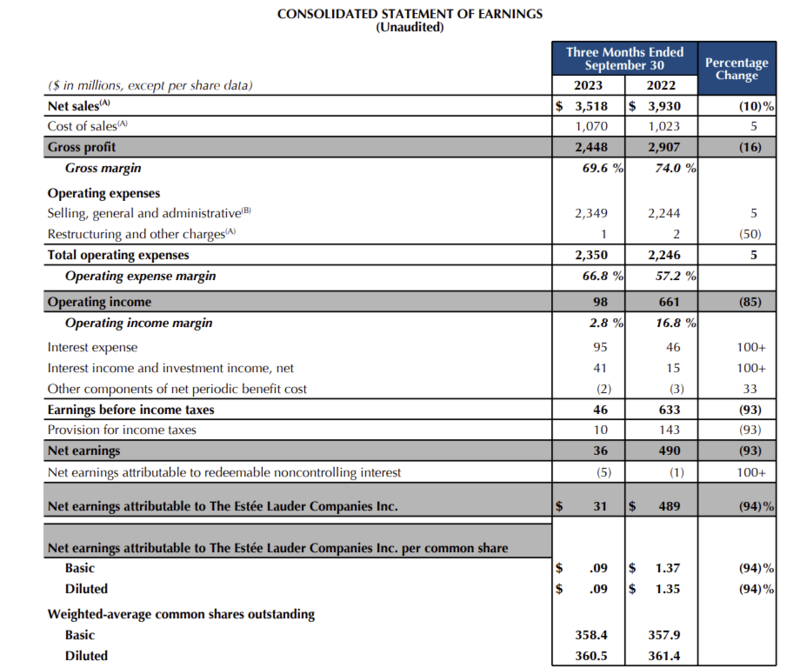

The company reported net earnings of US$31 million, down -94% compared with US$489 million in the prior year.

The decrease in operating income primarily reflected the decline in global travel retail net sales, strategic investments in advertising and promotional activities and higher in-store staffing expenses. These factors were partially offset by US$185 million of lower intercompany royalty expense due to the decline in income from the group’s travel retail business

“Another guidance cut with bottom perhaps finally found” – Goldman SachsCommenting on The Estée Lauder (EL) Companies’ Q1 results, Goldman Sachs Global Investment Research said in a note, “EL reported weak 1Q24 results (EPS beat on better margins but organic sales missed on a -11% decline) and cut its full year guidance meaningfully, primarily due to a lower China and Asia travel retail sales. “This follows three guidance reductions last year, which have understandably dented investor confidence. But at the risk of sounding over-optimistic, we were encouraged by much better than expected performance in the US by EL this quarter and believe the full year guidance has now been effectively de-risked. “We expect the debate about where earnings settle in FY25 to dominate discussions, but even if expectations fall to a $4-$5 range it is hard to argue for meaningful downside from where the stock is currently trading.” Goldman Sachs concluded: “We are Buy rated and our 12-month price target is $185, based on an equal weighted 30X P/E and 18X EV/EBITDA. Key risks to our rating and price target include a more protracted than expected recovery in Asia travel retail sales, a slower-for-longer performance of its US business, weaker than expected ongoing growth in Mainland China and/or greater cost to compete in China than we currently assume in our model.”

|

In a statement Freda said, “In the context of a quarter which we anticipated to be challenging, we delivered our organic sales outlook and exceeded expectations for profitability.

“Momentum continued in many developed and emerging markets around the world, where our organic sales grew strongly and we realised prestige beauty share gains. Encouragingly, we returned to growth in the US with fragrance, makeup and skincare all contributing. This performance partially offset the pressures of Asia travel retail and a slower recovery of overall prestige beauty in Mainland China.

“While we had a better-than-expected first quarter, we are lowering our fiscal 2024 outlook given incremental external headwinds, namely from the slower growth in overall prestige beauty in Asia travel retail and in Mainland China, which is currently confirmed in the pre-sale phase of the 11.11 Shopping Festival, and the risks of business disruption in Israel and other parts of the Middle East.

“We are accelerating and expanding our profit recovery plan, to benefit fiscal years 2025 and 2026, to realise our ambitions to rebuild profitability despite the external headwinds’ increased pressure on the business in fiscal 2024.”

Resetting retail inventory in Asia travel retail

Reflecting the challenges in Asia travel retail and Mainland China, ELC confirmed a lowering of its fiscal 2024 expectations for both markets. “Amid this headwind, the Company continues to expect to reset retailer inventory in Asia travel retail by the end of the third quarter of fiscal 2024,” ELC said.

“This, combined with the potential risks of further business disruptions in Israel and other parts of the Middle East as well as currency headwinds, are increasing the pressure on the Company’s fiscal 2024 financial results. With its revised outlook, the Company still anticipates to progressively improve performance in the second half of fiscal 2024.”

Skincare hard hit by Asia travel and Mainland China challenges

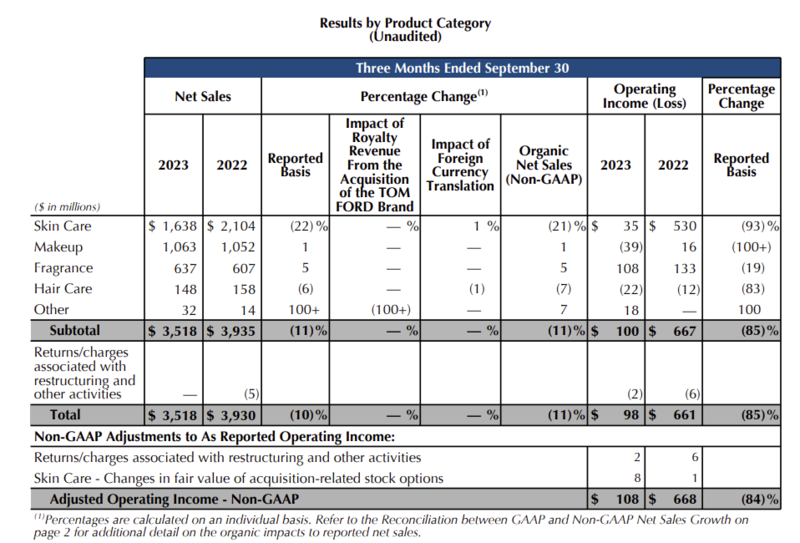

The travel retail and (partly related) Mainland China pressures played themselves out primarily in the key skincare category, where net sales decreased -21% year-on-year, with Estée Lauder and La Mer showing related declines.

Makeup net sales increased +1%, reflecting high-single-digit growth in the Americas and in Asia Pacific, partially offset by a decline in EMEA due to the Asia travel retail pressures (Asia travel retail forms part of EMEA).

Earnings call highlights – travel retail inventory reduction programme underway

During an earnings call, Fabrizio Freda and EVP and Chief Financial Officer Tracey Travis spelled out the Asia travel retail challenges and the road to recovery in the sector.

Freda highlighted one of four strategic imperatives outlined in the group’s August earnings call – i.e. to capture demand from returning individual travellers in Asia travel retail.

“For the first quarter, retail sales in global travel retail were substantially ahead of our organic sales decline, which reflects the execution of our priority to reduce trade inventory in alignment with retailers,” he commented.

“Indeed, we are making solid progress through exciting activation of our heroes, capitalising on innovation and investing in beauty advisers.”

Addressing a question about inventory headwinds, Travis said, “We expect organic sales for our second quarter to decline -8% to -10%. The incremental pressures from impacting sales in our Asia travel retail business and Mainland China are expected to continue to more than offset anticipated growth in other markets globally.

“Our retail trends are ahead of our net trends in Asia travel retail, both still down because we are destocking the trade. And so the expectation is that will be completed by the end of the third quarter.”

She continued: “We’re anniversarying from the second half of last year, where we had the policy changes first in Korea that impacted our third and fourth quarter and then the policy in Hainan, which impacted our fourth quarter. We had, in some parts of our travel retail business, very low shipments given those policy changes. And so we are anniversarying as well some of the initial shocks of that.”

Modest conversion rates

Speaking more broadly on the travel retail sector, Travis commented, “We are seeing travel come back… more slowly than what we anticipated. We are seeing lighter levels of conversion relative to what we saw certainly pre-pandemic or even pre- the significant changes in policy across the Asia region.

“But we are seeing traffic pick up, and we are certainly expecting that conversion will gradually pick up as well in the second half.”

Returning to the issue of inventory, Freda added: “In travel retail, we had a significant stock reduction in this first quarter. And we aim to be in line with the inventory expectation of retailers by the end of March. We have visibility into these numbers.

“We have exactly the understanding with each one of our retailers on where we are today, what are the programmes that we are doing in order to accelerate sales retail of the existing stocks and what are the programmes to replenish and sell in innovation and all what we need to do in these areas.

“And finally, how by the end of March, we aim to have the retail and the net aligned. That’s the programme.”

Shift from travel retail to China local market

Asked about rebuilding former groupwide profit margins in the faced of a reduced travel retail business, Travis noted that much former volume in the channel had shifted to local markets. “I would expect to continue to see growth in the local market as well. So there may be a rebalance as it relates to the consumption for the Chinese consumer in particular as well as perhaps other consumer groups,” she commented.

“So we’re not counting on travel retail to get back to prior levels. If it does, that’s great. But our profit recovery programme, combined with some of the growth plans that we have for our markets and brands going forward, are not relying on… the profit margins that we had previously.”

Commenting on the same theme, Freda added: “I would like to offer a bit of historical perspective on what happened during this COVID period and the volatility that this brought. Our business in Mainland China versus 2019 is more than doubled. Our TR business today globally versus 2019 is by now, with this estimate that we are giving to you now, actually well below.

“But it’s true that during this COVID period, the TR business – also driven by the unstructured phenomenon that we have discussed previously – was actually up. But then by now this has been reabsorbed.”

Normalisation of market structure “positive”

Freda said that the pandemic had transformed an estimated 40% of Chinese beauty consumption being made abroad (much of it in travel retail) in 2019 to a largely China-driven market due to frontier closures.

“Some of it went into travel retail, like the Hainan development and all the other things that happened, which are very good for the long term. And some of it went into the unstructured business, which is actually going down now and is part of the readjustment. And these are positive things for the long term.

“And so the result of all these movements is frankly solid and sustainable for the long term because the result is a solid business in Mainland China, which we are supporting and will continue to support,” Freda continued.

“We have built an R&D centre [in China]. We have created all the abilities to be more locally relevant in the future and to continue to support and invest in this business and invest in this very important market for us in the long term that we believe is core to our future growth algorithm.” ✈