AUSTRALIA/NEW ZEALAND. Ivo Favotto, a Sydney-based executive and company owner who has worked for all three stakeholders in the Trinity chain, presents his latest commentary and figures on the gradual re-emergence of airport commercial activities in Australia and New Zealand. Favotto owns and runs The Mercurius Group a consultancy focused on industry research, consultancy and benchmarking studies, as well as operating his own destination merchandise supply business. This month, he warns that the whole of 2021 may not see the levels of recovery hoped for, with vaccine programmes yet to start in either country and airport retail and F&B operators continuing to struggle with low passenger numbers that do not look like improving much any time soon.

As an eight-year-old, I remember being utterly terrified watching Jaws the movie when it first came out in 1975. It was – as director Steven Spielberg later described – “the definitive shark movie”. I had never been so scared in all my life – that is until three years later in 1978 when Jaws II was released with the tag line “just when you thought it was safe to go back in the water…”.

As an eight-year-old, I remember being utterly terrified watching Jaws the movie when it first came out in 1975. It was – as director Steven Spielberg later described – “the definitive shark movie”. I had never been so scared in all my life – that is until three years later in 1978 when Jaws II was released with the tag line “just when you thought it was safe to go back in the water…”.

And funnily enough, that Jaws II tagline came to mind when I reviewed the findings of The Mercurius Group’s tenth monthly report on the travel retail industry’s recovery from COVID-19 across Australia and New Zealand. Just when hope was giving way to optimism, the reality that is COVID-19 continues to strike fear into the travel retail community that the pain of 2020 might drag on well into 2021.

As last year came to a close there was some cautious optimism as both countries appeared to have effectively eliminated the virus and domestic traffic numbers were starting to recover. Alas, the virus returned with COVID-19 cases spreading out into the community – via staff working in hotel quarantine – causing the respective governments to start what is now a pattern of stop-start lockdowns and border closures.

“With the twin threats of continued dampened demand for travel and the cessation of wage subsidies, the travel retail industry is getting very nervous”

The sudden and brutal nature of shutdowns and border closures seems to be quickly eroding the public’s confidence to book travel. And all this is just referring to domestic travel – let’s not even talk about international travel.

International travel aspirations remain a very distant dream with vaccine programmes yet to start in either Australia or New Zealand. The schedule of vaccine delivery to the whole population is expected to take most of 2021 with governments in both countries making strong statements that they do not expect international borders to open until at least the end of the year.

Ongoing financial concerns are palpable in the Australian and New Zealand travel retail industry. Wage subsidies were effectively stopped in New Zealand in September 2020. Meanwhile, the Australian Federal Government has signalled the end to its COVID-19 wage subsidies in March 2021.

With the twin threats of continued dampened demand for travel and the cessation of wage subsidies, the travel retail industry is getting very nervous. Airports too are facing financial pressures, with the need to provide rent support to tenants on an ongoing basis. What every airport thought would be temporary relief is starting to become long-term financial support and may add to a growing list of longer term structural impacts on the landlord-tenant relationship.

With international travel appearing to be off the cards for the rest of 2021, travel retail operators (particularly duty free operators who are effectively 100% exposed) are faced with the reality of a second year of materially impaired trade, raising concerns about an exodus of operators from the region.

Australia and New Zealand had 56 million international passengers in 2019 and five duty free operators (Heinemann, Dufry, Lotte, ARI and LTR). A significant operator exodus won’t be good news for airports looking for some tender competition when the market does recover – noting that pre-COVID-19, there were a number of significant duty free concessions set to expire in 2022 (although these may have been extended during COVID-19 relief negotiations).

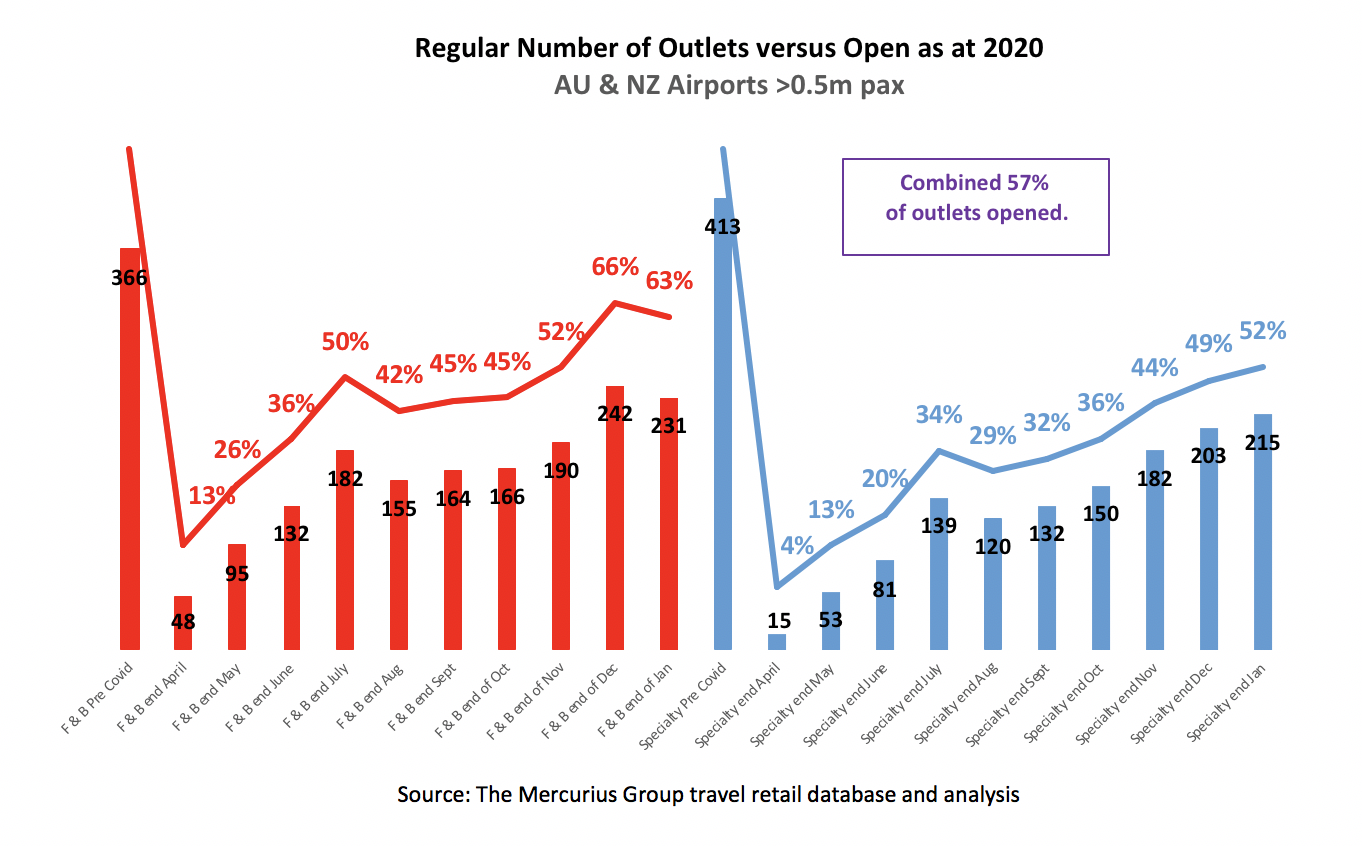

The Mercurius Group’s monthly reports on travel retail’s recovery from the health crisis in Australia and New Zealand records the reopening of 779 travel retail stores across the 27 airports with more than 0.5 million passengers across both countries.

January 2021 saw a consolidation in travel retail outlets open since the Melbourne shutdown dip in August, with just 57% of travel retail outlets open – the same percentage as December.

While specialty store reopenings were up slightly, F&B reopenings were down somewhat – yet another saw tooth (or shark tooth as the case may be) in the recovery chart. Although the number of travel retail outlets opened is at a post COVID-19 peak, this may be a “hollow high” as operators start to reconsider their previous eagerness to open as travelling numbers plummet due to intermittent border closures and the end of wage subsidies looming. As at the end of January 2021, there were still 333 outlets closed across Australia and New Zealand.

“The industry is now facing the reality that 2021 is not looking to be the year of recovery that was hoped for with the light of the end of tunnel looking to be another 12 months away”

Domestic terminals are – as expected – faring better than international terminals with just 30% of all travel retail outlets closed.

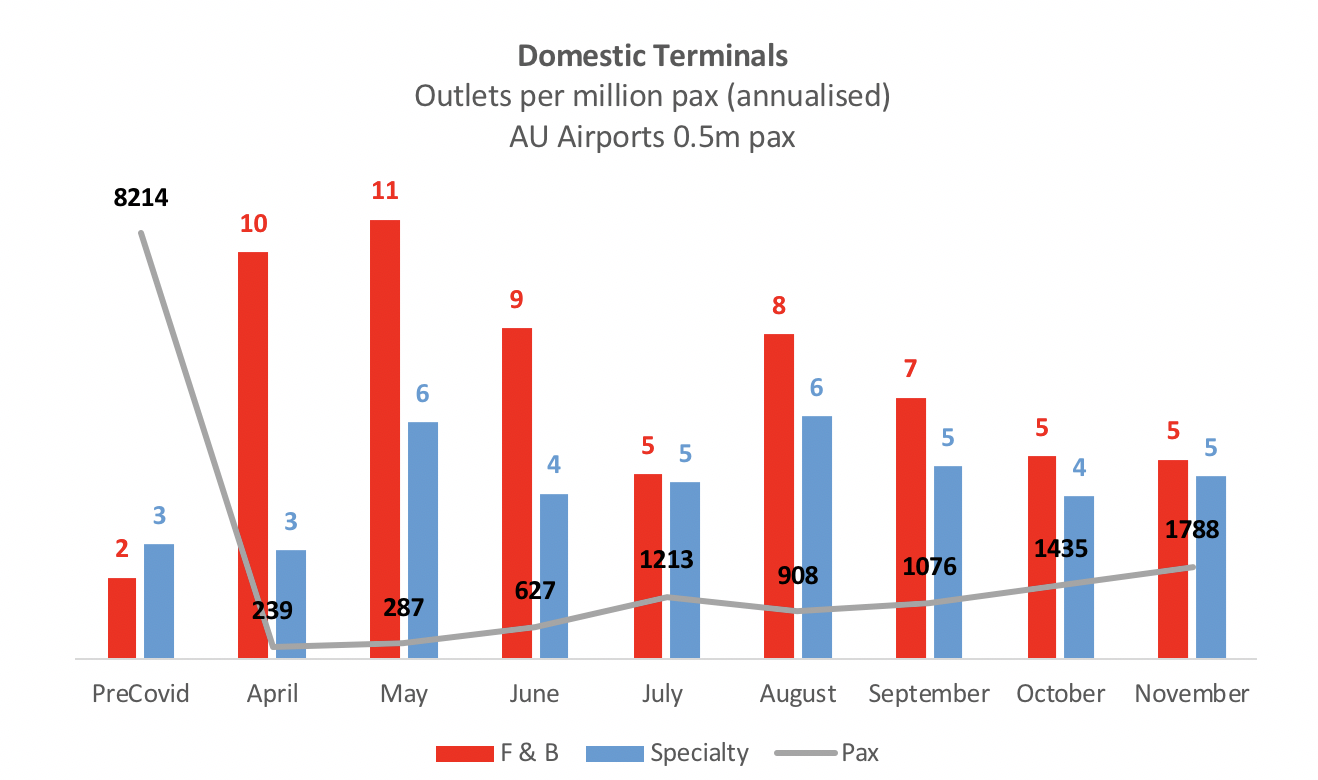

The reopening of outlets has to date continued to outpace the recovery in passengers. Noting that passenger statistics lag some months behind, in Australia domestic passenger numbers were just over 1.78 million in November 2020, down from around 9.56 million in the corresponding month in 2019.

In other words, in November 2020, 49% outlets were open and competing for business from just 19% of passengers compared to 2019. To date this mismatch in the equation has been supported by wage subsidies, flexibility in trading hours and the hope of rising passenger numbers. With the inputs to this equation under pressure, especially post-March, it can be expected that the number of stores open may fall once again unless traffic recovers quickly, though this seems increasingly unlikely.

Before the pandemic, on average domestic airports in Australia had two F&B and three specialty retail sites per million pax. As at the end of November, this was five outlets per million pax for F&B (two and half times more than usual) and five outlets per million pax for specialty (1.6 times more than usual).

Last month we talked about the potential consolidation of operators. We have also started to see some operators walking away from sites with F&B player Spotless’s departure from Gold Coast Airport being much talked about. While helpful in the current environment to the other incumbent operator – Airport Retail Enterprises – the Spotless departure is clearly symptomatic and potentially a portent of what is to come.

A long-term concern permeating discussions amongst all travel retailers is the longer term impact of human resourcing. Operators are reporting significant difficulty in recruiting customer services staff as work at an airport is seen as unreliable. At more senior levels, there is a talent drain due to layoffs, burnout and better opportunity elsewhere. When the recovery does start gathering pace there will be a significant challenge in getting teams up and running again.

![]()

The industry is now facing the reality that 2021 is not looking to be the year of recovery that was hoped for with the light of the end of tunnel looking to be another 12 months away – and even then, a full recovery is not predicted until 2024.

How profitable the industry will be may depend on the consolidation of operators and sites. Those that did get back into the water may have just spotted a shark’s fin starting to circle them.

Ivo Favotto contact: Tel: +61 423 564 057 Email: ifavotto@themercuriusgroup.com; Website: www.themercuriusgroup.com