Key take-outs – Currency issues in Argentina and Brazil hit hard in Q3 (driving organic sales growth decline of -0.7%, below consensus and the first negative result since Q2 2016); |

INTERNATIONAL. Dufry today unveiled what it described as “resilient” first nine-month results despite difficult recent market conditions in the key geographies of Spain, Argentina and Brazil (see full regional results breakdown in sidebar at foot of this page). Those challenges prompted an organic growth decline of -0.7% year-on-year in Q3.

The company claimed that efficiencies from its new Business Operating Model accelerated earlier than expected thus helping to drive further earnings growth and cash generation.

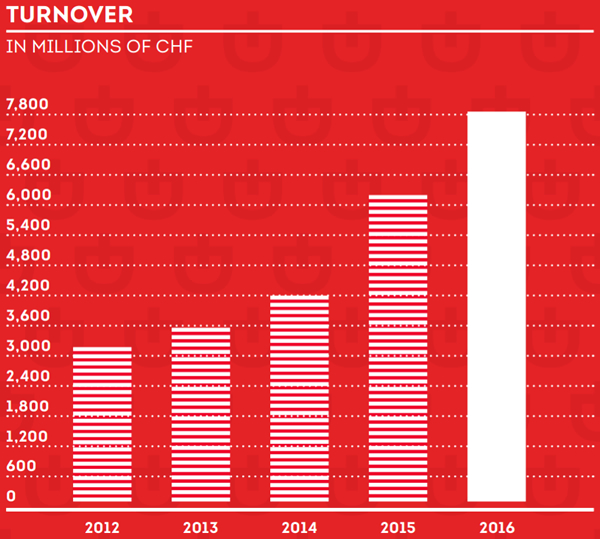

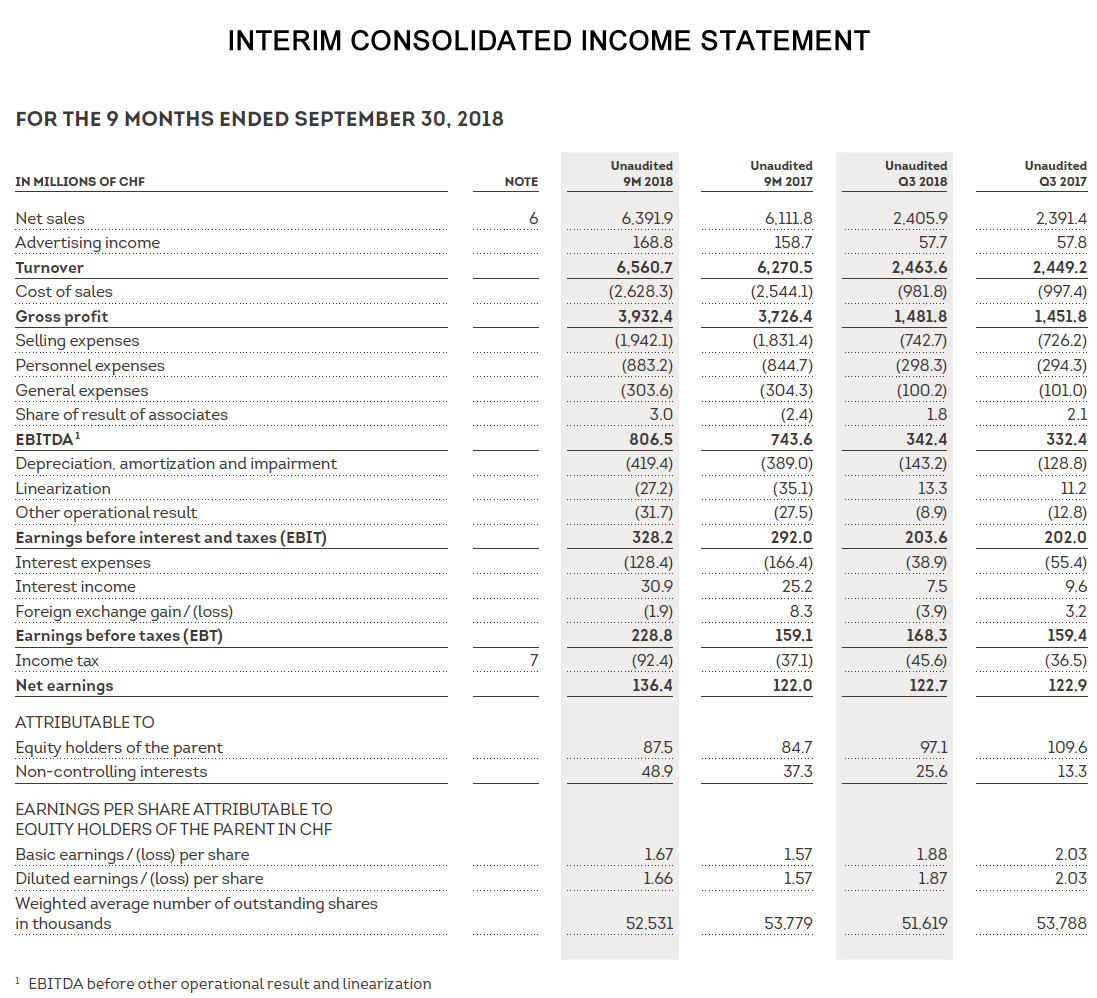

Reported turnover rose +4.6% to CHF6,560.7 million (US$6533.26 million), with organic growth up +3.1%.

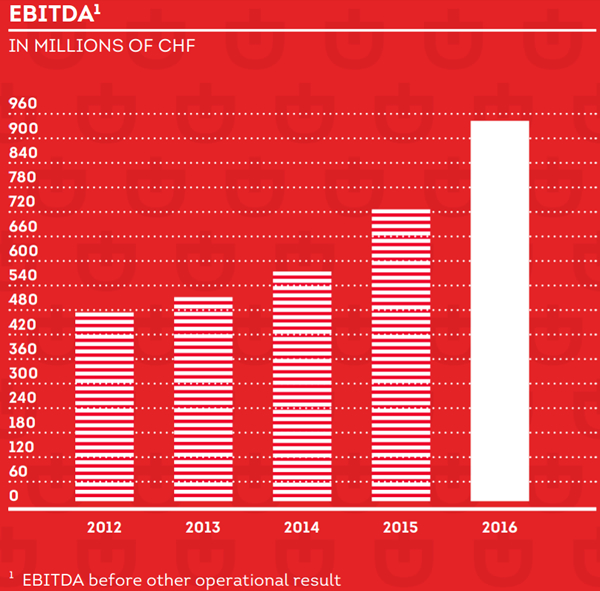

EBITDA rose +8.5% to CHF 806.5 million (US$803.1 million) with EBITDA margin increasing by 40 basis points year-on-year to 12.3%;

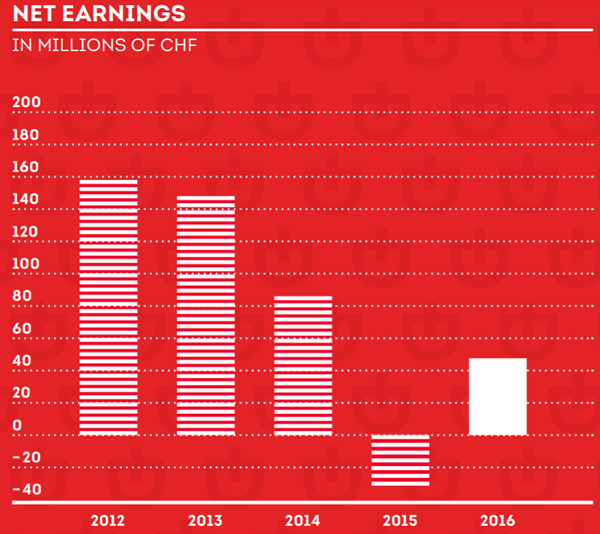

Cash EPS grew +4.5% to CHF6.07 (US$6.04). Free cash flow and equity free cash flow both grew strongly by +33.1% and +59.1% to CHF618.7 million (US$616.11)and CHF430.1 million (US$428.30 million) respectively.

Concession fees rise EBITDA margin expanded by 40 bps to 12.3% in the first nine months of 2018, compared with 11.9% last year. Apart from the expansion in the gross margin, the improvement came mainly as a result of the contributions from the BOM implementation, with a rationalisation of the cost structure generating savings in personnel and general expenses of 30 basis points year-on-year in the nine months. However, in an important observation, Dufry noted that selling expenses, 90% of which are concession fees, continued their trend upwards and rose by 40 basis points as a percentage of turnover in the nine months. This was due to the effect of the onerous Spanish airports contract, which is slightly above the normally expected range of 20-30 basis points per annum, the company said. |

Third-quarter headwinds

The retailer noted that in the third quarter “headwinds” had impacted trading in Spain, Brazil and Argentina. This resulted in a lower than anticipated turnover growth of +0.6% and in organic growth declining by -0.7% versus the same quarter last year;

The share buyback program of CHF400 million (US$398.33 million) was completed early (by 31 October).

Dufry Group CEO Julián Díaz commented: “Given the challenging market conditions being experienced in the wider retail sector and the ongoing volatility in some of the economies in which we operate, I am pleased to report that Dufry, with its strong position in the still growing sub-sector of travel retail, has delivered a resilient performance in the first nine months of 2018.

“In the first semester, we saw a good organic growth performance throughout the first and most of the second quarter in line with our initial expectations. With the beginning of the peak holiday season, we experienced a slowdown in organic growth driven by a shift of tourist flows from Spain to other Mediterranean destinations as well as a currency devaluation in Brazil and Argentina affecting the purchasing power of these important nationalities.

“The positive performance in our other operations could not fully compensate the impact of these geographies, thus resulting in an organic growth decline of -0.7% in Q3 2018 compared to the same period last year.

“Despite these impacts, we still expect a positive evolution of organic growth for the full year 2018 in the magnitude of between +2 and +3% supported by the important new openings.

“Despite these impacts, we still expect a positive evolution of organic growth for the full year 2018 in the magnitude of between +2 and +3% supported by the important new openings.

“The improvement [in gross profit margin] comes partly from a mix effect and mainly as a result of further renegotiations of terms and conditions with local suppliers, supported by a contribution from the acceleration of several brand plan initiatives, resulting either in better terms or higher advertising income.” – Dufry

“Looking at our three key financial metrics, we continued to generate top-line growth in most of our operations, driven mainly by organic growth. Our EBITDA margin expanded by a further 40 basis points to 12.3%; and we managed to generate significant improvement in both our free cash flow and equity free cash flow which increased to CHF618.7 million and CHF430.1 million respectively.

“Being a global company, we have once again seen differences in the performance of our several operations, a trend that will continue due to the diverse nature of our portfolio. Whilst Spain, Brazil and Argentina experienced headwinds linked to specific local issues, most of our other operations in the UK, Central and Eastern Europe, the Middle East, Asia and North America continued to grow.

“The implementation of the Business Operating Model (BOM) is now in its final phase. The efficiencies outlined earlier can already be seen coming through in our financials, being an important element of the EBITDA margin improvement in the period. We expect to see the full efficiencies being realised in the next few quarters.

“After generating CHF 195 million (US$194.8 million) synergies from the acquisitions of Nuance and WDF, the BOM is a clear example on our capability to extract additional savings and become a more efficient company.

“Despite the headwinds in selected markets, Dufry has a strong strategic positioning with a broad portfolio of high-quality concessions across many markets in a sector with positive fundamentals.

“Our focus continues to be the delivery of solid long-term results for our shareholders.”

OPERATIONAL HIGHLIGHTS

Dufry highlighted its acceleration of the Business Operating Model (BOM) implementation with CHF33.0 million (US$32.86 million) already reflected in the nine-month results.

Around CHF40 million (US$39.83 million) of efficiencies is expected to be reflected in total in FY2018 and the remaining CHF10 million (US$9.9 million) BOM efficiencies to come in 2019.

Trading update & full year outlook Dufry said that over the last few years it has evolved into a substantially larger and more diversified business, “better positioned for the future and with enhanced opportunities in both existing and new travel retail markets”. It continued: “Despite the headwinds in certain countries – in particular with the structural [concession fee -Ed] issues in Spain, and to a lesser extent in Brazil and Argentina – which are likely to persist for the coming quarters, Dufry’s business model and the fundamentals of the travel retail market do remain solid.” The company said that, based on current indications of trading during October, it anticipates some stabilisation of the business in the fourth quarter and a potential improvement in the fourth quarter compared to the third. In the first four weeks of October net sales had gradually improved; with organic growth close to+1%. That improvement was due to several factors including lower exposure to Spain; the annualisation of the closing of the Dufry operation at Geneva Airport (October 2017); further improved performance in Asia; and the contribution of new openings, namely in Hong Kong and Australia. “We remain focused on cost control and plan to complete the implementation of the Business Operating Model, which will be important for the EBITDA development in the next few quarters,” said Dufry. “We therefore expect to see an outcome for the full year 2018 that will demonstrate continuing year-on-year progress for the overall Group.” Organic growth is now expected to be in a range of between +2% and +3%; EBITDA margin between 12.0% and 12.3%; with equity free cash flow of between CHF350 million and CHF400 million being confirmed. |

A continued refurbishment of operations across the Group to improve customer experience and maximise sales resulted in 27,700sq m being refurbished in the first nine months of the year. This total included the implementation of the ‘New Generation Store’ concept at Heathrow Airport T3 (2,500sq m) and Cancún T3 (1,800sq m) as well as the main store in Glasgow Airport and several stores at Málaga and Ngurah Rai International (Bali) airports.

Some 18,300sq m of gross new retail space opened in the reporting period including the start of operations onboard 13 cruise ships, totalling close to 4,000sq m across 41 stores.

Key duty free operations opened at the MTR high-speed railway station in Hong Kong (three stores – 1,500sq m) and covering 36 stores across several operations in North America (adding 3,500sq m).

Contracts are now signed to open a further 16,100sq m of new space in 2018 and 2019, including operations already opened in October at the new Jazeera terminal at Kuwait Airport and 1,400sq m of duty free retail space at Perth Airport, Australia (with a further 1,300sq m to come in 2019).

FINANCIAL RESULTS IN DETAIL

Within the +4.6% turnover increase, like-for-like growth contributed with +1.8% and net new concessions added +1.3%, which resulted in organic growth of +3.1%.

The FX translation effect during the full period was 1.5%, mainly due to the strengthening of the Euro and the British Pound versus the Swiss Franc.

Within the third-quarter turnover growth of +0.6%, revenues declined by -0.9% on a like-for-like basis, compared to an increase of +3.5% in H1 2018, due to the weaker trading largely in Spain, Argentina and Brazil.

Net new concessions also contributed less during the period with 0.2% in the third quarter from +2.0% in H1 2018, as several of the concessions that provided positive contribution annualised. As a result, organic growth was -0.7% in the third quarter.

The FX translation effect was positive at 1.3% for the third quarter, as the US Dollar, Euro and Pound Sterling strengthened year-on-year versus the Swiss Franc.

MARGIN ENHANCEMENT

Dufry said that further negotiations with suppliers had driven improvement in the gross profit margin, which improved by 50 basis points in the first nine months to 59.9%, compared to 59.4% in the previous year.

“The improvement comes partly from a mix effect and mainly as a result of further renegotiations of terms and conditions with local suppliers, supported by a contribution from the acceleration of several brand plan initiatives, resulting either in better terms or higher advertising income,” Dufry said.

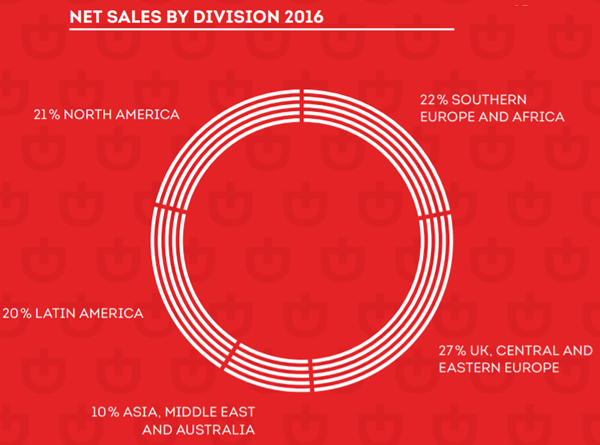

A MIXED REGIONAL PICTURE Southern Europe and Africa: Turnover in this region grew by +1.6% to CHF1,456.3 million, (US$1,451 million) with organic growth falling by -2.1%. In the third quarter organic growth slowed to -5.2%. Spain had the weakest performance, noted Dufry. This was due to “an unfavourable passenger nationality mix affecting spend per passenger and tougher comparatives on the record numbers of international tourists in the previous years, which were substituted with domestic passengers”. The company said: “While our operations in Turkey and to a lesser extent Greece benefited from the shift of tourists from Spain, the improvement seen here did not fully offset the Spanish impact. Italy, France and Malta all continue with good organic growth.” UK and Central Europe: Turnover amounted to CHF1,484 million (US$1,478.8 million) in the period, +2.5% higher than the same period last year. Organic growth, excluding the impact of the from the duty free concession in Geneva, amounted to an “encouraging” +3.6%; including Geneva, organic growth fell by -0.7% for the nine months. Organic growth was higher in the third quarter at +0.2%, mainly due to an acceleration of growth in the UK, which accounts for about two-thirds of this business and where several operations benefited from refurbished stores and “intensified in-store marketing efforts”, said Dufry. Performance continued to be solid in Switzerland and Sweden, while Finland was flat, added the company. Eastern Europe, Middle East, Asia and Australia: Turnover increased to CHF849.5 million (US$848.5 million) with strong organic growth of +15.2%. In the third quarter organic growth was +4.4%, a good performance against the high comparables of the previous year, according to Dufry. Within the division, Russia maintained the solid recent performance and Bulgaria, Serbia and Armenia all enjoyed “good growth”. In the Middle East most operations saw double-digit growth (Jordan, Kuwait and India). Sharjah also continued with its positive performance. In Asia, where performance has been strong for a number of quarters, growth ran at a lower rate, although it remained solid in Macau, Cambodia and South Korea. Australia continued to perform well, with strong double-digit performance driven by the full renovation of the Melbourne Airport stores. Latin America: Performance here reflected the “challenging market conditions” resulting from extreme currency volatility in the largest markets, namely Brazil and Argentina. Here, noted Dufry, the devaluation of the respective local currencies versus the US Dollar impacted sales. Other operations in South America slowed in the third quarter, a knock-on effect from these two key countries, the company added. While turnover for the first nine months of 2018 fell by -2.8% to CHF1,212.6 million (US$1,208 million), organic growth fell by -11.0% in the third quarter. Performance in Central America, including the Caribbean, continued to be strong, especially in the cruise division, which saw high double-digit growth. Mexico was the exception, flat in the third quarter after a strong H1 2018. North America: Turnover increased by +6.6% to CHF1,415.1 million (US$1,410 million), compared to the first nine months of 2017. Organic growth reached +7.5% in the period and +7.1% in Q3, with strong like-for-like growth generated by healthy passenger numbers and good contributions from net new concessions, said Dufry. |